Impulse spending is defined as any unplanned purchase driven by emotion rather than need. Americans spend an estimated $314 monthly on impulse buys, which adds up to nearly $3,800 each year in unplanned costs. The good news is that you can reduce impulse spending habits without relying on willpower alone. Proven methods like the 72-hour waiting rule, cognitive behavioral therapy (CBT) techniques, and intentional friction strategies address the root causes of impulsive buying. This guide gives you the exact steps to control impulsive buying, manage emotional triggers, and build financial habits that actually stick.

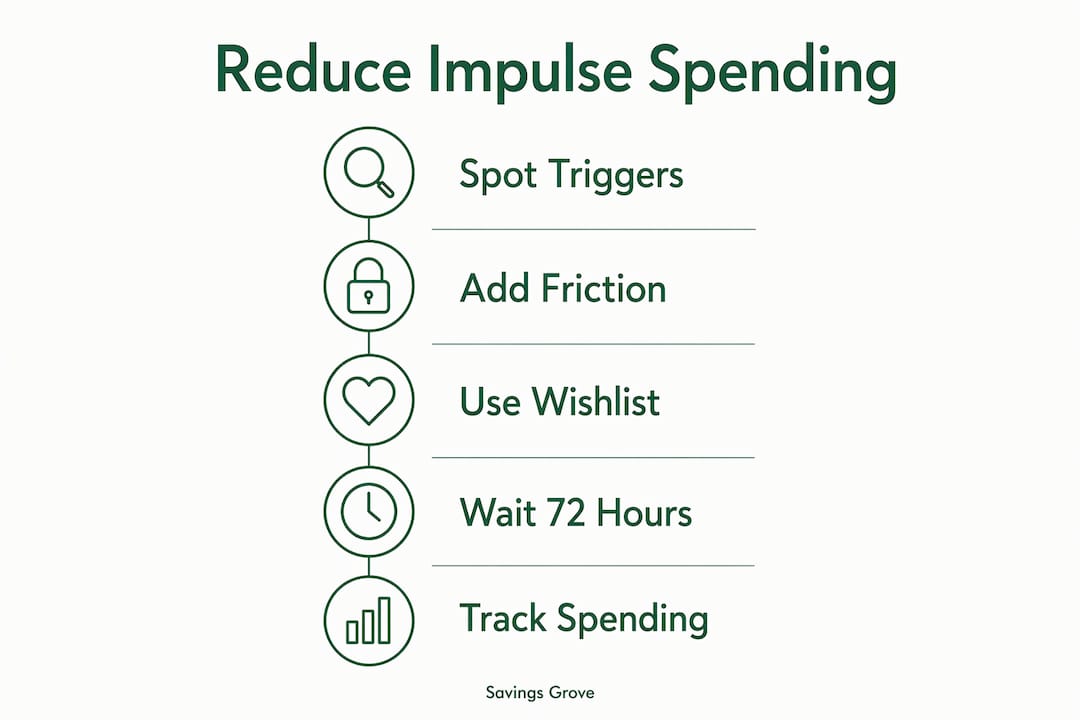

What triggers impulse spending and how do you spot them?

Impulse spending is less about weak willpower and more about mismanaged emotional responses. Boredom, stress, loneliness, and social pressure are the most common emotional states that push people toward unplanned purchases. Recognizing your personal triggers is the first step toward changing the behavior.

Retail environments are designed to exploit these emotional states. Present bias and urgency tactics like “limited time offer” banners and low-stock warnings make you feel that buying now is safer than waiting. These mechanisms bypass rational thinking and activate the brain’s reward system, making a purchase feel satisfying before you have time to evaluate it.

Keeping a spending journal is one of the most effective ways to identify your personal patterns. Write down every unplanned purchase, the time of day, your emotional state, and what triggered the urge. After two weeks, clear patterns will emerge. You might notice you shop online most often after stressful work calls, or that you browse retail apps when you are bored on weekends.

A written wishlist serves a similar purpose. Keeping a purchase log separates emotional desire from reasoned buying decisions, reducing regret and unnecessary spending. When you write down what you want instead of buying it immediately, you give yourself time to evaluate whether the item actually fits your life and budget.

- Boredom and stress: These two states account for the majority of emotional impulse purchases. Identify the times of day or week when you feel most vulnerable.

- Social pressure: Seeing friends or influencers display purchases creates a sense of urgency to keep up. Unsubscribing from promotional emails can reduce impulse spending by over $1,000 per year on average.

- Environmental cues: Store layouts, app notifications, and email promotions are all engineered to trigger buying. Removing these cues from your environment reduces exposure before the urge even starts.

Pro Tip: Set your phone to “Do Not Disturb” during your highest-risk shopping hours. If you know you browse retail apps after 9 PM, that single change can eliminate dozens of impulse opportunities each month.

How does intentional friction help you overcome impulse purchases?

Intentional friction means adding small obstacles between the urge to buy and the act of purchasing. These obstacles give your rational brain time to catch up with your emotional brain. The results are significant. Applying a 72-hour waiting rule leads to about 73% of impulse purchases being abandoned entirely. That translates to approximately $2,400 in annual savings for the average American.

The mechanics are straightforward. When you feel the urge to buy something unplanned, add it to a wishlist or note app instead of your cart. Set a reminder to revisit the item after 72 hours. Most of the time, the emotional charge behind the purchase will have faded by then, and you will decide you do not actually need it.

Online shopping requires specific friction tactics because the purchase path is designed to be frictionless. Removing stored credit card information and deleting shopping apps from your home screen disrupts the one-click checkout reward loop. Even 30 seconds of added friction measurably decreases impulse transactions. Moving apps to a secondary screen or requiring manual card entry forces a pause that breaks the automatic reflex.

In-person shopping has its own set of friction tools. Grocery shoppers who use prepared lists spend 23% less than those who shop without one. Never shop when you are hungry, tired, or emotionally activated. These states lower your resistance to in-store marketing tactics and increase the likelihood of unplanned purchases.

| Friction method | How it works | Expected impact |

|---|---|---|

| 72-hour waiting rule | Delays purchase decision by 3 days | Eliminates ~73% of impulse buys |

| Remove saved payment info | Requires manual card entry at checkout | Breaks automatic purchase reflex |

| Delete shopping apps | Removes one-tap access to retail platforms | Reduces browsing-triggered purchases |

| Use a shopping list | Limits in-store decisions to pre-planned items | Cuts grocery spend by ~23% |

| Unsubscribe from promo emails | Reduces marketing exposure at the source | Saves over $1,000 annually on average |

Pro Tip: Use a free browser extension that replaces retail homepage images with a photo of your financial goal. Seeing your goal every time you open a shopping site reframes the decision before you even start browsing.

What behavioral techniques build long-term spending control?

Surface-level tactics work best when paired with deeper behavioral change. CBT-based methods address the emotional patterns that drive impulsive buying, making your progress more durable over time. The average American makes about 3 impulse purchases weekly, totaling more than $5,400 annually. Changing that pattern requires more than rules. It requires rewiring how you respond to emotional discomfort.

Here are four behavioral techniques that produce lasting results:

-

Urge surfing. Urges to spend act like waves that peak and recede. Urge surfing is a CBT strategy that teaches you to observe the urge without acting on it. When you feel the impulse, name it out loud or in writing: “I feel the urge to buy this jacket.” Then wait. The urge will peak within a few minutes and fade on its own. Each time you ride it out, the urge becomes easier to manage.

-

If-then planning. Write out specific plans for your highest-risk situations. “If I feel stressed after work, then I will go for a 20-minute walk instead of opening a shopping app.” This technique removes the need for in-the-moment decision-making, which is when impulse control is weakest.

-

Replace spending with non-monetary coping. Exercise, meditation, and social connection are effective alternatives to emotional spending. These activities address the underlying emotional need without the financial cost. If you understand the connection between emotional triggers and behavior, you can apply the same substitution logic to spending urges.

-

Allocate guilt-free spending money. Overly strict budgets create rebound spending. Budgets that include planned fun money reduce impulsive rebound purchases. Set aside a fixed amount each month for discretionary spending with no rules attached. When that amount is gone, it is gone. This structure satisfies the desire for spontaneity without derailing your financial goals.

“Values-driven spending is more sustainable than restrictive rules alone. When you align your purchases with what genuinely matters to you, the urge to buy things that do not fit your priorities loses its power.” — behavioral finance research on intentional spending habits

Tracking your spending in real time reinforces all of these techniques. Use a budgeting app or a simple spreadsheet to log every purchase the moment it happens. Awareness alone shifts behavior. When you see your discretionary spending total climb in real time, you naturally become more selective. Pair this with a financial minimalism mindset to further clarify which purchases genuinely add value to your life.

How do you handle common setbacks when curbing spending?

Progress rarely moves in a straight line. Most people encounter predictable obstacles when they first try to control impulsive buying, and knowing what to expect makes those obstacles easier to manage.

- Social pressure from friends or family. Shopping outings and group purchases create real pressure to spend. Prepare a short, neutral response: “I’m working on a savings goal right now.” You do not owe anyone a detailed explanation. Having the phrase ready removes the awkwardness of deciding what to say in the moment.

- Marketing tactics that feel personal. Retargeted ads follow you across websites after you browse a product. These ads are not a sign that you need the item. They are a sign that the algorithm tracked your behavior. Recognizing this mechanism helps you dismiss the ad rather than act on it.

- Rebound spending after strict restrictions. Cutting all discretionary spending cold turkey almost always leads to a spending binge within weeks. Gradual reduction works better than total elimination. Cut one category at a time and replace the spending with a planned alternative.

- Loss of motivation over time. Tie your savings goal to something specific and visible. A photo of your target goal on your phone’s lock screen keeps the reason for your discipline front and center. Savings Grove’s guide on cutting household expenses offers concrete milestones you can use to track progress.

Pro Tip: Schedule a monthly “spending review” on your calendar. Reviewing your wins and setbacks once a month keeps you accountable without the daily pressure of tracking every decision.

Digital tools add another layer of support. Spending alert features in most banking apps notify you when you approach a category limit. Turning these alerts on creates an automatic check-in that does not require any willpower on your part. Pair alerts with automatic savings transfers to move money out of your checking account before you have a chance to spend it impulsively.

Key Takeaways

Reducing impulse spending requires combining intentional friction, emotional awareness, and behavioral substitution to produce lasting financial change.

| Point | Details |

|---|---|

| Use the 72-hour rule | Waiting 3 days before buying eliminates about 73% of impulse purchases. |

| Add friction to online shopping | Remove saved payment info and delete shopping apps to break automatic buying reflexes. |

| Identify your emotional triggers | Keep a spending journal to spot the emotional states and times that drive unplanned purchases. |

| Apply CBT techniques | Urge surfing and if-then planning address root causes, not just symptoms. |

| Allow planned discretionary spending | A guilt-free spending budget prevents rebound purchases that follow overly strict restrictions. |

What I have learned about impulse spending the hard way

By Mika L.

The most useful shift I made was stopping the search for more willpower and starting to look at my environment instead. I used to think impulse purchases were a character flaw. They are not. They are a predictable response to emotional states and engineered retail environments. Once I accepted that, I stopped feeling ashamed and started making practical changes.

The 72-hour rule felt awkward at first. I thought I would forget about items I genuinely needed. What actually happened was that I forgot about most of them, and that told me everything I needed to know. The items I still wanted after three days were the ones worth buying.

The hardest part was not the tactics. It was self-compassion. Slipping up and making an impulse purchase does not erase your progress. It gives you data. Ask yourself what triggered it, what you were feeling, and what you could do differently next time. That reflection is more valuable than any app or rule. Treat impulses as information, not failure, and the whole process becomes far less exhausting.

— Mika L.

How Savings Grove helps you manage your money better

Building better spending habits is easier when you have the right resources in one place.

Savings Grove is a personal finance platform built for people who want practical, research-backed guidance without the jargon. The site covers everything from frugal living strategies to credit card rewards and budgeting tools, all updated monthly with fact-checked information. Whether you are working on curbing unplanned purchases or building your first real budget, Savings Grove gives you the tools and knowledge to make progress. Visit Savings Grove to explore resources that match where you are in your financial life right now.

FAQ

What is the fastest way to stop impulse buying?

The 72-hour waiting rule is the most effective single tactic. Applying it consistently eliminates about 73% of impulse purchases and saves approximately $2,400 annually.

Why do I keep buying things I do not need?

Impulse purchases are driven by emotional triggers like stress, boredom, and social pressure, not by actual need. Retail environments are engineered to exploit these states using urgency and social proof tactics.

How much does impulse spending cost the average American?

Americans spend an estimated $314 per month on impulse buys. The average American makes about 3 impulse purchases per week, totaling more than $5,400 annually.

Does having a budget stop impulse spending?

A budget helps, but only if it includes a planned discretionary amount. Budgets with no fun money tend to trigger rebound spending. Allocating a fixed guilt-free amount each month reduces the urge to overspend.

What is urge surfing and how does it reduce impulse purchases?

Urge surfing is a CBT technique where you observe a spending urge without acting on it, allowing it to peak and fade naturally. Practicing it regularly builds the ability to pause between the urge and the purchase decision.