Dividend income is defined as the regular cash payments a company distributes to shareholders from its profits, and the role of dividend income in retirement is to supply retirees with reliable payouts that cover living expenses without forcing them to sell investments. A sustainable portfolio yield for retirees sits around 3%, with annual dividend growth of 3.5% needed to maintain purchasing power over time. Fidelity recommends a 4%–5% initial withdrawal rate adjusted for inflation across a 30-year retirement horizon, blending dividend income with growth assets and fixed income to reduce risk. For retirees and pre-retirees, understanding how dividends fit into a broader financial plan is the first step toward building real income security.

How does dividend income support retirement financial security?

Dividends generate cash flow even when markets fall. That single fact separates dividend income strategy in retirement from pure growth investing, where you must sell shares to fund expenses. Selling shares during a downturn locks in losses. Dividends let you hold your positions and wait for recovery.

Dividends reduce the need to sell shares at depressed prices during market downturns, buffering what financial planners call sequence-of-return risk. Sequence-of-return risk is the danger that early retirement losses permanently shrink your portfolio before it has time to recover. Keeping shares intact during downturns means you benefit fully when markets rebound.

Dividend growth also fights inflation. A company that raises its dividend by 5% per year gives you a pay raise every year, something a fixed bond coupon never does. Quality dividend payers provide inflation protection through consistent dividend growth, a feature bonds generally lack. That distinction matters enormously over a 20 or 30-year retirement.

Dividend investing provides psychological reassurance to retirees through a “smooth ride” of consistent cash flow, even when total return lags. Regular income reduces the emotional pressure to react to market swings. That calm is worth more than most retirees expect.

Pro Tip: Set up automatic dividend reinvestment during your pre-retirement years, then switch to cash payouts at retirement. This one change converts your growth engine into an income engine without selling a single share.

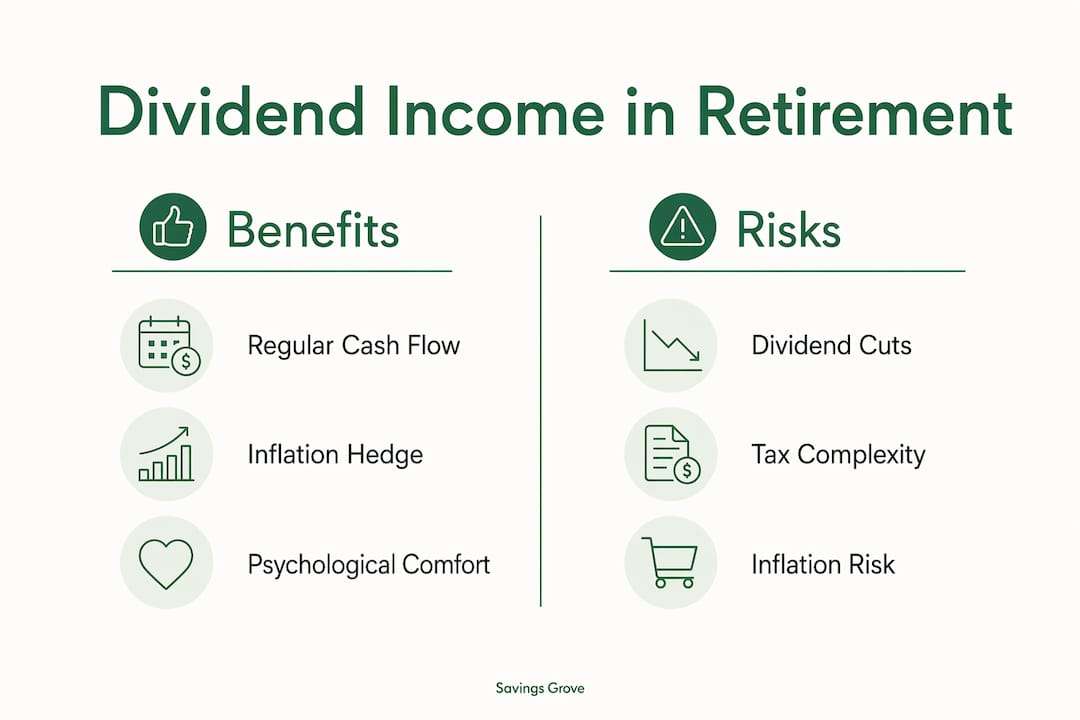

Key benefits of dividend income for retirees include:

- Income without selling. Dividends pay you while you hold, preserving your principal base.

- Inflation protection. Dividend growth stocks can raise payouts faster than inflation rises.

- Lower volatility. Dividend-focused portfolios tend to experience smaller price swings than pure growth portfolios.

- Psychological comfort. Predictable deposits reduce anxiety during volatile markets.

- Flexibility. You can reinvest or spend dividends based on your current needs.

What are the risks of relying solely on dividends for retirement income?

Dividend income is powerful, but it is not a complete retirement plan on its own. Retirees who depend entirely on dividends expose themselves to several real risks that can erode financial security over time.

The most dangerous trap is yield chasing. High dividend yield alone is often a warning sign of potential dividend cuts and underlying business weakness, not an attractive buying opportunity. A 10% yield on a struggling company is not income. It is a countdown to a dividend cut and a falling share price.

Tax treatment adds another layer of complexity. Dividends create taxable income in the year received, which can complicate retirement tax planning compared to capital gains strategies. Growth portfolios let you control when you realize gains. Dividends arrive on the company’s schedule, not yours, which can push you into a higher tax bracket unexpectedly.

Concentration risk is also a serious concern. Dividend-paying stocks cluster in sectors like utilities, real estate investment trusts, and consumer staples. Overweighting these sectors leaves your portfolio vulnerable if one industry faces regulatory changes or economic pressure.

Watch for these warning signs in a dividend-focused portfolio:

- Payout ratio above 80%. A company paying out most of its earnings has little room to sustain dividends during a downturn.

- Dividend yield significantly above sector average. This often signals the market expects a cut.

- Declining free cash flow. Dividends paid from debt rather than earnings are not sustainable.

- Heavy sector concentration. More than 40% in any single sector increases risk without proportional reward.

- No dividend growth history. A flat dividend over five or more years loses ground to inflation every year.

Relying solely on dividends can lead to a fixed-income lifestyle that fails to keep pace with inflation over decades. Dividend portfolios targeting 3%–5% yields often need supplementation for growth. That is not a flaw in dividend investing. It is an argument for combining dividends with a broader total return approach.

How to create a balanced retirement income strategy with dividends

A balanced retirement income strategy treats dividends as one engine in a larger machine, not the only one. A total return approach involving dividends, interest income, and selective asset sales provides better diversification and adaptability than dividend-only strategies. Dynamic withdrawal methods built on this framework can extend portfolio longevity significantly.

Here is a practical framework for building that balance:

- Estimate your income target. Calculate your annual spending needs, then subtract guaranteed income like Social Security or pensions. The gap is what your portfolio must cover.

- Size your portfolio correctly. Multiply your desired annual dividend income by 22 to 28 to estimate the portfolio size needed to generate it sustainably. A $40,000 annual income target requires a portfolio of roughly $880,000 to $1,120,000 at a 3% yield.

- Apply a sustainable withdrawal rate. Start at 4%–5% and adjust annually for inflation, following Fidelity’s guidance for a 30-year horizon.

- Build a bucket structure. Keep one to two years of expenses in cash or short-term bonds, dividend income in a mid-term bucket, and growth assets in a long-term bucket.

- Rebalance annually. Trim overweight positions and redirect proceeds to underweight areas to maintain your target allocation.

- Consider dynamic withdrawal rules. The Guyton-Klinger method adjusts withdrawals based on portfolio performance, cutting spending slightly in bad years and allowing increases in good ones.

Pro Tip: Place dividend-paying stocks in tax-advantaged accounts like a Roth IRA or traditional IRA when possible. This defers or eliminates the annual tax drag on dividend income and gives your portfolio more room to compound.

| Income source | Role in retirement portfolio | Key benefit |

|---|---|---|

| Dividend income | Regular cash flow from equities | Covers expenses without selling shares |

| Bond interest | Stable fixed income | Reduces overall portfolio volatility |

| Selective asset sales | Fills income gaps as needed | Provides tax timing flexibility |

| Social Security | Guaranteed baseline income | Reduces portfolio withdrawal pressure |

For retirees interested in low-risk investment options, combining dividend stocks with Treasury bonds creates a foundation that balances income and stability. Savings Grove covers both approaches in detail for 2026.

How to select quality dividend stocks and funds for retirement

Selecting the right dividend investments separates a sustainable income stream from a fragile one. The goal is not the highest yield. The goal is the most reliable and growing yield over time.

Focus on dividend growth stocks rather than high-yield stocks. A company that has raised its dividend for 10 or more consecutive years demonstrates the financial discipline and business strength that retirees need. The S&P 500 Dividend Aristocrats index tracks companies with 25 or more consecutive years of dividend increases, making it a useful starting screen.

Evaluate these criteria before buying any dividend investment:

- Free cash flow coverage. The dividend should be well covered by free cash flow, not just earnings. Cash flow is harder to manipulate than reported earnings.

- Debt levels. Companies carrying heavy debt loads are more likely to cut dividends during economic stress.

- Dividend growth rate. A 5%–7% annual growth rate compounds powerfully over a 20-year retirement.

- Sector diversification. Spread holdings across healthcare, consumer staples, industrials, and financials to avoid sector-specific shocks.

- Fund options. Dividend-focused exchange-traded funds and mutual funds offer instant diversification and professional selection for retirees who prefer not to pick individual stocks.

Account placement also matters. Qualified dividends taxed at the long-term capital gains rate belong in taxable accounts. Non-qualified dividends taxed as ordinary income belong in tax-deferred accounts. Getting this placement right can meaningfully reduce your annual tax bill. Retirees managing senior investment risk should review account placement as part of their annual financial checkup.

Key Takeaways

Dividend income works best in retirement when combined with a total return strategy, proper portfolio sizing, and disciplined withdrawal rules rather than used as a standalone income source.

| Point | Details |

|---|---|

| Sustainable yield target | Aim for a 3% portfolio yield with 3.5% annual dividend growth to preserve purchasing power. |

| Portfolio sizing rule | Multiply desired annual income by 22–28 to estimate the portfolio size you need. |

| Withdrawal rate guidance | Start withdrawals at 4%–5% annually and adjust for inflation over a 30-year horizon. |

| Avoid yield chasing | High yields often signal dividend cuts; prioritize dividend growth history over current yield. |

| Tax placement matters | Hold high-yield dividend payers in tax-advantaged accounts to reduce annual tax drag. |

Why dividend income changed how I think about retirement risk

Mika L., Senior Financial Writer

Most retirement advice treats dividend income as a bonus. I think that framing is backwards. The real value of dividends is not the cash itself. It is the discipline it forces on both the companies paying them and the retirees receiving them.

When I started studying dividend strategies seriously, I expected to find a simple income solution. What I found instead was a behavioral tool. Mental accounting leads retirees to treat dividend income separately from principal, which lowers the psychological friction of spending in retirement. That is genuinely useful. Retirees who feel comfortable spending their dividends are less likely to underspend and sacrifice quality of life out of fear.

The mistake I see most often is treating dividend income as a fixed salary. It is not. Dividends can be cut. Companies change. Sectors fall out of favor. The retirees who do best are the ones who use dividends as a foundation and stay flexible about everything else. They hold money tips for seniors close and revisit their strategy every year, not every decade.

My honest recommendation: build your dividend income to cover 60%–70% of your essential expenses, then use a total return approach to cover the rest. That ratio gives you the psychological comfort of predictable income while keeping enough flexibility to adapt when markets or life circumstances change.

— Mika L.

How Savings Grove supports your retirement income planning

Retirement income planning works best with current, practical resources at your side.

Savings Grove publishes monthly updates on dividend income strategies, portfolio construction approaches, and retirement income tools built specifically for retirees and pre-retirees. The site covers dividend yield targets, withdrawal rate guidance, and tax-efficient account placement in plain language. Whether you are building your first dividend portfolio or refining an existing one, Savings Grove gives you the research-backed guidance you need to make confident decisions. Visit Savings Grove to access the latest strategies and start building a retirement income plan that fits your life.

FAQ

What is the role of dividend income in retirement?

Dividend income supplies retirees with regular cash payments from their investments, covering living expenses without requiring them to sell shares. It reduces sequence-of-return risk and supports financial stability during market downturns.

How much portfolio do I need to live off dividends?

Multiply your desired annual dividend income by 22 to 28 to estimate the required portfolio size at a 3% sustainable yield. A $50,000 annual income target requires roughly $1.1 million to $1.4 million in dividend-paying assets.

Are dividends guaranteed in retirement?

Dividends are not guaranteed. Companies can cut or eliminate payouts during business downturns, which is why diversification and dividend growth history matter more than current yield alone.

How are dividends taxed in retirement?

Dividends create taxable income in the year received, regardless of whether you spend them. Qualified dividends are taxed at the lower long-term capital gains rate, while non-qualified dividends are taxed as ordinary income.

Should I rely only on dividends for retirement income?

Relying solely on dividends risks falling behind inflation and limits tax flexibility. A total return strategy combining dividends, bond interest, and selective asset sales provides better long-term sustainability for most retirees.