Treasury bonds are long-term U.S. government securities that pay fixed interest semiannually until maturity, giving seniors a dependable source of retirement income backed by the full faith and credit of the federal government. The role of treasury bonds for seniors goes well beyond simple savings. These fixed income investments provide predictable cash flow, protect principal when held to maturity, and serve as a stabilizing force inside a retirement portfolio. For retirees managing monthly expenses on a fixed budget, that combination of safety and consistency is hard to match.

How do treasury bonds provide reliable income for seniors?

Treasury bonds deliver income through a fixed coupon rate paid every six months. You know exactly how much you will receive and exactly when. That predictability is the core reason treasury bonds for retirees work so well as a cash flow tool.

Treasury bonds are sold in 20-year or 30-year maturities. When you hold a bond to its maturity date, the U.S. Treasury returns your full principal. No guessing, no market timing required.

Here is what a simple income schedule looks like in practice. A retiree who purchases $50,000 in treasury bonds at a 4.5% coupon rate receives $2,250 per year, paid in two installments of $1,125 every six months. Stack several bonds with staggered purchase dates, and you can create a near-monthly income stream.

Compare that to other fixed income options:

- Treasury bonds: Fixed coupon, U.S. government backed, principal returned at maturity

- Corporate bonds: Higher yields but carry credit risk and are not government guaranteed

- Certificates of deposit (CDs): FDIC insured but typically shorter terms and subject to renewal rate risk

- Annuities: Guaranteed income but often carry high fees and limited liquidity

- Dividend stocks: Variable income with market price risk, unsuitable as a primary income source for conservative retirees

Pro Tip: Purchase bonds at different times throughout the year so your semiannual payments land in different months. This spreads your income more evenly across the calendar.

What risks and limitations should seniors consider?

Treasury bonds carry real risks that every retiree should understand before investing. Knowing these risks does not mean avoiding bonds. It means using them correctly.

-

Interest rate risk. Rising rates reduce the market value of existing long-term treasury bonds. If you sell before maturity, you may receive less than you paid. Holding to maturity eliminates this risk entirely.

-

Inflation risk. A fixed coupon that pays 4% loses real purchasing power when inflation runs at 5%. Standard treasury bonds do not adjust for inflation. Treasury Inflation-Protected Securities (TIPS) address this, but they are a separate product.

-

Federal income tax. Interest earned on treasury bonds is subject to federal income tax. That income counts toward your adjusted gross income and can affect Medicare premium calculations under IRMAA thresholds.

-

State and local tax exemption. Treasury bond interest is exempt from state and local income taxes. For retirees in high-tax states like California, New York, or New Jersey, this exemption meaningfully improves after-tax returns compared to corporate bonds.

-

Capital gains tax. If you sell a treasury bond in the secondary market before maturity at a price above what you paid, the gain is taxable. Selling at a loss creates a deductible capital loss.

Common misconception: Many retirees assume treasury bonds are completely risk-free. They are credit-risk-free, meaning the U.S. government will not default. But they carry interest rate risk and inflation risk. Understanding that distinction helps you use them appropriately.

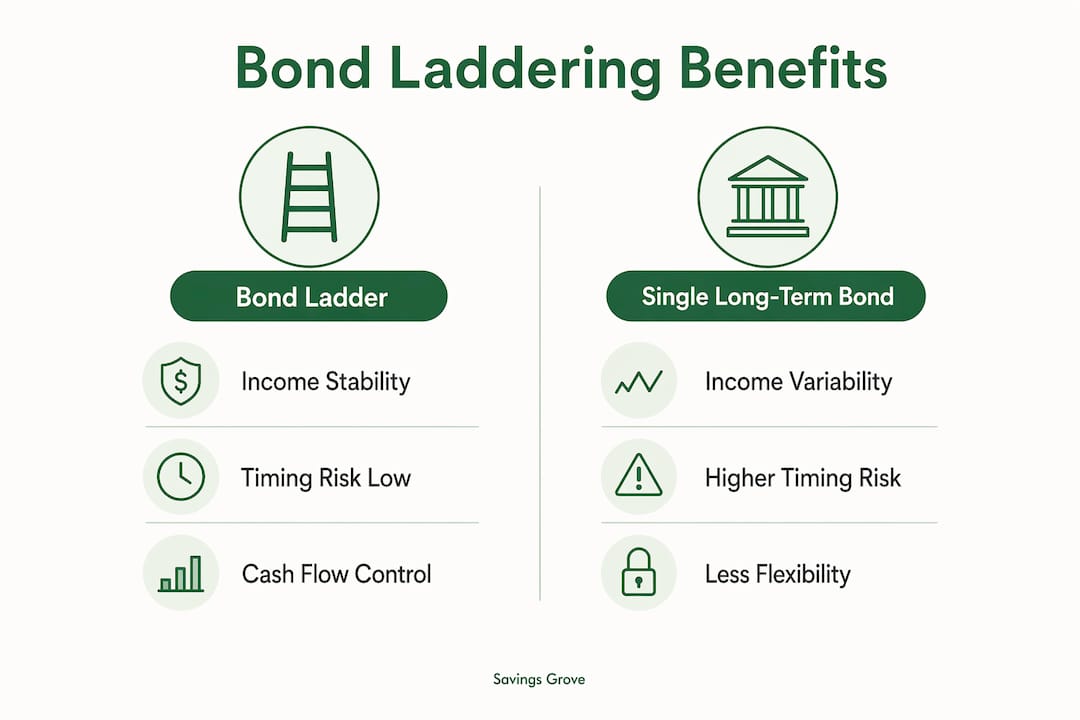

How can seniors use bond laddering to improve retirement income stability?

Bond laddering is the single most practical strategy for retirees investing in treasury bonds. A ladder staggers bond maturities across multiple years so that a portion of your principal returns on a regular schedule.

Bond laddering helps retirees manage cash flow and minimize timing risk. Instead of locking all your money into one 30-year bond at today’s rate, you spread purchases across bonds maturing in 1, 2, 3, 5, and 10 years. Each maturity gives you a decision point: spend the principal, reinvest at current rates, or shift to a different asset.

Bond ladder vs. single long-term bond: a direct comparison

| Feature | Bond ladder | Single long-term bond |

|---|---|---|

| Timing risk | Low. Maturities spread across years | High. All principal tied up until one date |

| Rate flexibility | High. Reinvest at current rates as bonds mature | None until maturity |

| Income predictability | Consistent across multiple intervals | Fixed but concentrated |

| Liquidity | Partial liquidity at each maturity | Limited without selling at market price |

| Complexity | Moderate. Requires planning | Simple. One purchase |

Retiree portfolios often allocate 1–3 years of spending needs to short-duration Treasuries or cash. This approach funds near-term withdrawals without forcing you to sell longer bonds at an unfavorable market price.

The key discipline is reinvestment. Retirees must commit to reinvesting maturing bonds rather than shifting maturity profiles based on short-term rate movements. Changing the ladder opportunistically defeats the purpose.

Pro Tip: Start your ladder with TreasuryDirect.gov, the U.S. Treasury’s official platform. You can purchase bonds directly without broker fees, which preserves more of your return.

How do treasury bonds fit within a broader retirement portfolio?

Treasury bonds act as a stability tool rather than a yield maximizer inside a retirement portfolio. That distinction matters. You are not buying Treasuries to outperform the stock market. You are buying them to protect against it.

Fidelity research highlights that Treasuries provide portfolio ballast during genuine risk-off environments, meaning periods when stock prices fall sharply. When equities drop, retirees who hold Treasuries can draw income from bond payments instead of selling stocks at depressed prices. That protection preserves long-term portfolio value.

Individual treasury bonds held to maturity offer principal certainty that bond funds cannot match. Bond funds have no fixed maturity date, so their market values fluctuate continuously with interest rates. For retirees who need to know exactly what they will have at a specific date, individual bonds are the more reliable choice.

Practical allocation considerations for seniors:

- Risk-averse retirees (age 75 and older, limited other income): A heavier allocation to short and intermediate Treasuries reduces volatility and protects spending power.

- Tax-advantaged accounts: Holding Treasuries inside a traditional IRA defers federal tax on interest. Holding them in a Roth IRA makes that interest completely tax-free.

- Taxable brokerage accounts: The state and local tax exemption on treasury interest still applies, making Treasuries more tax-efficient than corporate bonds in these accounts.

- Balanced portfolios: A mix of Treasuries, dividend-paying stocks, and a small allocation to TIPS covers income, growth, and inflation protection across different market conditions.

The right allocation depends on your spending needs, Social Security income, other assets, and tax situation. A fee-only financial advisor can help you size the Treasury portion correctly for your specific retirement plan.

Key Takeaways

Treasury bonds serve seniors best as a predictable income source and portfolio stabilizer, not as a tool for maximum yield.

| Point | Details |

|---|---|

| Reliable semiannual income | Fixed coupon payments every six months give retirees a consistent, predictable cash flow. |

| Hold to maturity for safety | Selling before maturity exposes you to interest rate risk. Holding eliminates that risk entirely. |

| State tax exemption adds value | Treasury interest is exempt from state and local taxes, improving after-tax returns in high-tax states. |

| Bond laddering reduces timing risk | Staggered maturities let you reinvest at current rates and access principal on a regular schedule. |

| Treasuries stabilize portfolios | During stock market downturns, Treasury income reduces the need to sell equities at low prices. |

What I have learned about treasury bonds and retirement income

By Mika L.

After years of reviewing retirement portfolios and talking with retirees about their financial concerns, one pattern stands out clearly. Most seniors underestimate how much peace of mind a simple bond ladder provides. They focus on yield comparisons and miss the bigger picture: knowing that $10,000 is coming back to you in 18 months, no matter what the stock market does, changes how you make every other financial decision.

The most common mistake I see is buying a single long-term treasury bond and treating it as a set-and-forget solution. That works fine if you never need the money early. But life rarely cooperates with a 30-year plan. A ladder gives you flexibility without sacrificing safety.

The tax angle surprises many retirees too. If you live in a state with a high income tax rate, the state exemption on treasury interest is not a minor footnote. It is a real, calculable advantage over corporate bonds that deserves a place in your planning conversation.

My honest recommendation: pair your treasury ladder with a conversation with a fee-only financial advisor who specializes in retirement income. The international treasury management strategies that institutional investors use are increasingly accessible to individual retirees. You do not need a large portfolio to benefit from disciplined bond allocation. You need a clear plan and the patience to stick with it.

— Mika L.

Savings Grove and your retirement income plan

Retirement income planning works best when you have clear, current information in one place. Savings Grove tracks investment opportunities, fixed income strategies, and money-saving tools updated monthly so you always have accurate guidance.

Whether you are building your first treasury bond ladder or reviewing an existing retirement portfolio, Savings Grove provides the research and comparisons you need. The site covers retirement savings strategies alongside credit card rewards, savings account rates, and practical tips that add up over time. Seniors who take a structured approach to retirement income consistently make better decisions with their money. Savings Grove gives you the resources to do exactly that.

FAQ

What are treasury bonds and how do they work?

Treasury bonds are long-term U.S. government debt securities sold in 20-year or 30-year maturities. They pay a fixed interest rate every six months and return your full principal at maturity.

Are treasury bonds safe for seniors?

Treasury bonds are backed by the full faith and credit of the U.S. government, making them free of credit risk. They carry interest rate risk if sold before maturity, but holding to maturity eliminates that concern.

How is treasury bond interest taxed for retirees?

Treasury bond interest is subject to federal income tax but exempt from state and local income taxes. Retirees in high-tax states benefit most from this exemption compared to other fixed income options.

What is a bond ladder and why does it help retirees?

A bond ladder staggers treasury bond maturities across multiple years so principal returns on a regular schedule. This reduces timing risk and lets retirees reinvest at current rates as each bond matures.

Should seniors hold individual treasury bonds or bond funds?

Individual treasury bonds held to maturity provide principal certainty that bond funds cannot offer. Bond funds fluctuate in market value with interest rates and have no fixed maturity date, which creates uncertainty for retirees with specific cash flow needs.