Low-risk investment options for retirees are financial products designed to preserve capital while generating reliable retirement income. The core category includes FDIC-insured accounts, U.S. Treasury securities, Treasury Inflation-Protected Securities (TIPS), and fixed annuities. Each product serves a different purpose, but all share the same goal: protecting what you have built while keeping money flowing in. This guide covers the safest vehicles available in 2026, how to balance liquidity with yield, and how to build a portfolio that holds up against inflation, interest rate shifts, and unexpected expenses.

What are the best low-risk investment options for retirees?

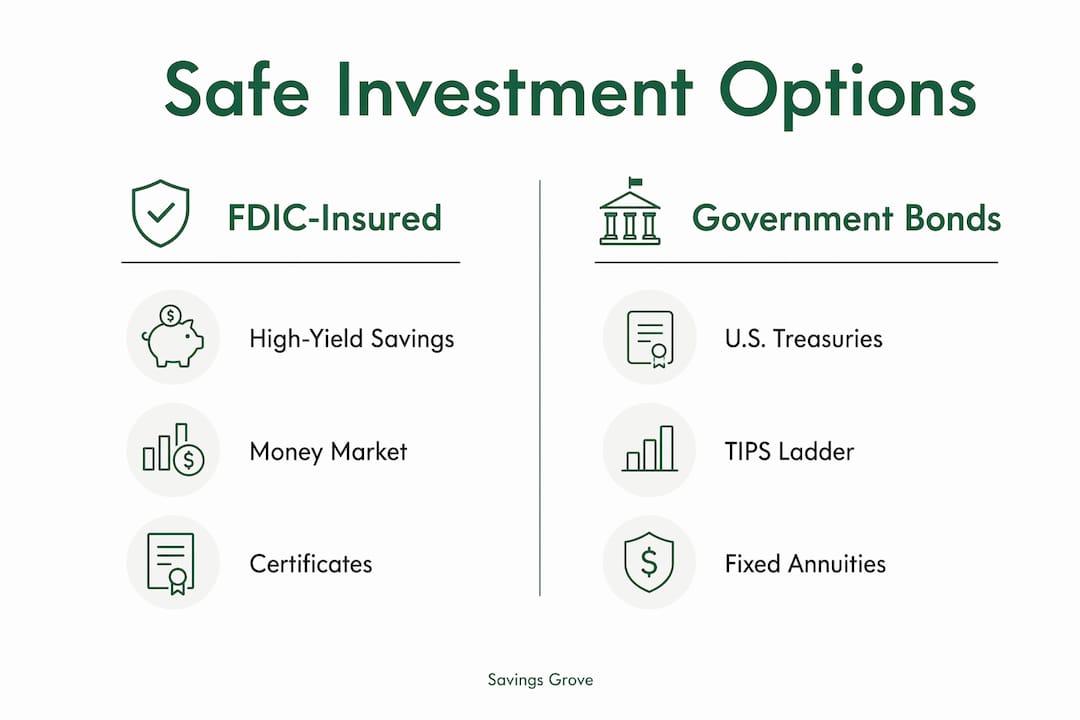

The safest conservative investments for retirees fall into three broad categories: FDIC-insured deposit accounts, U.S. government securities, and fixed annuities. Understanding what each one does, and what it costs you in flexibility, is the foundation of sound financial planning for retirement.

FDIC-insured accounts

FDIC-insured accounts include high-yield savings accounts, money market accounts, and certificates of deposit (CDs). The FDIC protects up to $250,000 per depositor, per bank, per ownership category. That limit matters more than most retirees realize. Two accounts at the same bank may not both be fully insured unless they fall into different ownership categories. A married couple can protect well over $1,000,000 by using individual, joint, payable-on-death (POD), and retirement account categories correctly, without needing a complicated trust structure.

Pro Tip: Use the FDIC’s free EDIE estimator tool at FDIC.gov to check whether your current account setup is fully covered before you deposit another dollar.

U.S. Treasury securities

U.S. Treasuries are among the safest investments available to retirees because the federal government backs every dollar. Treasury bills mature in under a year. Treasury notes run 2–10 years. Treasury bonds extend to 30 years. TIPS, or Treasury Inflation-Protected Securities, adjust their principal with inflation, which makes them particularly useful for retirees worried about purchasing power erosion over a long retirement.

Fixed annuities

Fixed annuities are contracts with insurance companies that guarantee a set interest rate for a defined period. They offer predictable income, but they come with surrender charges if you withdraw early. They are not FDIC-insured, so the strength of the issuing insurance company matters. Check the insurer’s financial strength rating through agencies like AM Best before committing.

Quick comparison of core safe investment choices

| Product | Access | Yield potential | Key risk |

|---|---|---|---|

| High-yield savings account | Immediate | Moderate (4%+) | Rate can drop anytime |

| CD | Locked until maturity | Moderate to good | Early withdrawal penalty |

| U.S. Treasury securities | Liquid in secondary market | Low to moderate | Interest rate price swings |

| Fixed annuity | Restricted (surrender period) | Moderate | Insurer credit risk |

How does liquidity affect your choice of safe retirement investments?

Liquidity is the ability to access your money without a penalty or a loss. For retirees, it is not optional. Unexpected medical bills, home repairs, and family needs do not wait for a CD to mature.

The key difference between CDs and high-yield savings accounts comes down to penalties. High-yield savings accounts offer competitive yields with no early withdrawal penalty, while CDs lock your money in for a fixed term. CBS News reported in june 2026 that savings accounts can offer rates above 4% while still giving you same-day access to funds. That combination makes them a strong first layer in any low-risk asset allocation for retirees.

Here is a practical framework for balancing liquidity with yield:

- Keep three to six months of living expenses in a high-yield savings account or money market account. This is your emergency buffer, and it should never be locked up.

- Use short-term CDs (3–12 months) for predictable near-term expenses. If you know you will need money in six months for a planned trip or a tax payment, a short CD captures a better rate than a savings account without much risk.

- Ladder CDs across multiple maturities. Stagger CDs so one matures every few months. This gives you regular access to cash while keeping the rest earning a higher rate.

- Reserve longer-term instruments for money you will not need for five or more years. Treasury notes, TIPS, and fixed annuities belong in this bucket.

Pro Tip: Online banks and credit unions frequently offer the highest rates on high-yield savings accounts. Check Savings Grove’s monthly rate updates at savingsgrove.com to compare current offers before opening a new account.

How do bond ladders and TIPS strategies generate steady retirement income?

A diversified low-risk portfolio for retirees does more than hold safe assets. It structures those assets so income arrives predictably and inflation does not quietly eat it away. Two tools stand out for doing this well: bond ladders and TIPS ladders.

The TIPS ladder strategy

A TIPS ladder is a series of individual TIPS bonds, each maturing in a different year, so you receive a payment annually or at regular intervals. Morningstar’s 2026 research shows a 30-year TIPS ladder delivers a simulated withdrawal rate of 4.8% while providing inflation-adjusted income fully secured by the U.S. government. That rate is meaningful because it comes without the market timing risk that stock-heavy portfolios carry.

The critical rule with a TIPS ladder is to hold each bond to maturity. Selling TIPS before maturity exposes you to market price swings and removes the inflation protection the strategy depends on. The ladder only works as designed when you let it run its course.

Bond ladders with nominal bonds

A traditional bond ladder uses Treasury notes or investment-grade corporate bonds staggered across maturities of 1, 2, 3, 5, and 7 years. Each year, the shortest bond matures and you reinvest at the current rate. This approach manages interest rate risk by spreading your exposure across time rather than betting on one rate environment.

Short and intermediate bonds carry less price volatility than long bonds. That matters because fixed income investments carry real risks, including interest rate changes that move bond prices in the opposite direction. A bond ladder limits that damage by ensuring you always have bonds maturing soon, reducing the need to sell at a loss.

Combining tools for a complete income portfolio

| Strategy | Income type | Inflation protection | Liquidity |

|---|---|---|---|

| TIPS ladder | Inflation-adjusted annual payments | Strong | Low (hold to maturity) |

| Nominal bond ladder | Fixed periodic payments | None | Moderate |

| High-yield savings account | Variable interest | Partial (rate-dependent) | High |

| Fixed annuity | Guaranteed fixed payments | None to low | Low |

A well-built retirement income portfolio often combines all four. You can also add a small allocation to dividend-paying stocks or balanced funds for growth, which financial planners sometimes call an “equity kicker.” That growth component offsets the purchasing power loss that purely fixed income portfolios face over a 20 to 30-year retirement. For a broader look at safe retirement investment types, combining instruments across categories is the standard approach among conservative planners.

What risks remain even with low-risk retirement investing?

“Low risk” does not mean “no risk.” Fidelity identifies four distinct risks in fixed income investing that retirees must understand before building a portfolio.

- Interest rate risk. When interest rates rise, bond prices fall. If you need to sell a bond before it matures, you may receive less than you paid. Shorter maturities reduce this exposure significantly.

- Credit risk. This is the risk that an issuer defaults on payments. U.S. Treasuries carry essentially no credit risk. Corporate bonds and fixed annuities carry more, depending on the issuer’s financial health.

- Inflation risk. A fixed payment worth $1,000 today buys less in 10 years if inflation runs at 3% annually. TIPS and I-Bonds address this directly. Nominal bonds and fixed annuities do not.

- Liquidity risk. Some bonds trade in thin markets, meaning you may not find a buyer quickly or at a fair price. This is less of a concern with Treasuries, which trade in one of the deepest markets in the world, but it matters for smaller corporate bond issues.

Retirees should evaluate each investment by its specific risk type rather than treating all low-risk products as equivalent. A CD carries no credit risk and no interest rate price risk if held to maturity, but it carries inflation risk and liquidity risk. A TIPS bond eliminates inflation risk but introduces interest rate price risk if sold early. Knowing which risk you can least afford to take guides you toward the right mix. For a practical guide on building a diversified retirement portfolio, matching instruments to specific risks is the starting point.

Conservative retirement portfolios that combine FDIC-insured accounts, Treasuries, bonds, and annuities stabilize income and preserve capital better than any single instrument alone. Diversification does not eliminate risk, but it prevents one bad outcome from derailing your entire income plan.

Key Takeaways

The most effective low-risk retirement income strategy combines FDIC-insured accounts, TIPS ladders, and bond ladders to address inflation, liquidity, and interest rate risks simultaneously.

| Point | Details |

|---|---|

| FDIC coverage requires structure | Use individual, joint, POD, and retirement account categories to maximize insured amounts per bank. |

| TIPS ladders protect against inflation | A 30-year TIPS ladder delivers a 4.8% simulated withdrawal rate with government-backed inflation protection. |

| Liquidity belongs in your plan | Keep three to six months of expenses in a high-yield savings account before locking money into CDs or annuities. |

| Hold bonds to maturity | Selling TIPS or bond ladder holdings early exposes you to market price swings and removes key protections. |

| Low risk is not no risk | Credit, interest rate, inflation, and liquidity risks all exist in fixed income. Match each instrument to your specific risk tolerance. |

What I have learned about playing it safe in retirement

By Mika L.

Most retirees I talk with assume that moving into safe investments means accepting low returns and calling it a day. That assumption costs them more than they realize. The real skill in retirement income planning is not just picking safe products. It is matching the right product to the right purpose.

I have seen retirees park everything in CDs because they felt safe, only to watch inflation quietly reduce their purchasing power year after year. I have also seen retirees hold long-term bond funds thinking they were conservative, then panic when rates rose and fund values dropped. Both mistakes come from treating “low risk” as a single category rather than a spectrum.

My honest recommendation is to build in layers. Start with a fully insured cash buffer in a high-yield savings account. Add a TIPS ladder for your core living expenses, sized so each rung covers one year of spending. Fill the gap between your Social Security income and your actual expenses with that ladder. Then use a short to intermediate bond ladder for discretionary spending. If you have money beyond those needs, a small equity allocation keeps your portfolio growing without putting your income at risk.

Review the whole picture once a year, not just when markets move. Rates change, your expenses change, and your risk tolerance changes. A portfolio that fit you at 65 may need adjusting at 72. Work with a fee-only financial advisor who has no incentive to sell you products. The combination of insured cash, TIPS, and a bond ladder is not exciting, but it works.

— Mika L.

How Savings Grove helps retirees find the right safe investments

Retirement investing does not have to be confusing. Savings Grove researches and updates financial products monthly so you can compare high-yield savings accounts, CDs, and other safe options without spending hours on it yourself.

Savings Grove tracks current rates on FDIC-insured accounts and highlights which products offer the best combination of safety and yield for retirees. Whether you are setting up your first cash buffer or comparing CD terms, the tools and resources at Savings Grove give you clear, current information to make confident decisions. No guesswork, no sales pressure. Just straightforward guidance built for retirees who want their money to work safely and steadily.

FAQ

What is the safest investment for retirees in 2026?

U.S. Treasury securities and FDIC-insured accounts are the safest options available. Both carry government backing and protect against issuer default.

How much does FDIC insurance cover per account?

The FDIC insures up to $250,000 per depositor, per bank, per ownership category. A married couple using multiple account types can protect well over $1,000,000 at a single bank.

Are high-yield savings accounts better than CDs for retirees?

High-yield savings accounts offer similar or higher yields than CDs with no early withdrawal penalty, making them better for retirees who need flexible access to funds.

What is a TIPS ladder and how does it help retirees?

A TIPS ladder is a series of Treasury Inflation-Protected Securities maturing in different years, providing annual inflation-adjusted income. Morningstar’s 2026 research shows a 30-year TIPS ladder supports a 4.8% simulated withdrawal rate when bonds are held to maturity.

Can a retiree lose money in low-risk investments?

Yes. Low-risk does not mean risk-free. Interest rate changes, inflation, and early sale of bonds can all reduce the value of fixed income holdings. Diversifying across multiple instruments limits that exposure.