Financial literacy is defined as the combination of knowledge, attitudes, skills, and behaviors that enables a person to make sound financial decisions. The OECD measures financial literacy across three core dimensions: financial knowledge, financial behavior, and financial attitudes. Understanding financial literacy means going far beyond knowing what a savings account is. It means applying that knowledge to real choices about spending, saving, debt, and investing. For most Americans, that gap between knowing and doing is where financial stress lives.

What is financial literacy and what does it actually include?

Financial literacy is the practical ability to manage money well across four core areas: budgeting, saving, debt management, and investing. The OECD definition makes clear that literacy is not just about knowing financial products. It combines attitudes (how you feel about money), behaviors (what you actually do), and knowledge (what you understand). All three must work together for real financial progress.

Each area covers specific skills:

- Budgeting: Tracking income and expenses, setting spending limits, and adjusting when circumstances change.

- Saving: Building an emergency fund, setting savings goals, and automating contributions.

- Debt management: Understanding interest rates, minimum payments, and the true cost of carrying a balance.

- Investing: Grasping concepts like compound interest, risk tolerance, and diversification.

A common misconception is that financial literacy means memorizing financial products or terms. Mastering budgeting, saving, debt, and investing sets a foundation that improves every financial decision you make after that. Knowing what a Roth IRA is does not make you financially literate. Using one consistently and understanding why it fits your goals does.

Pro Tip: Start by writing down every dollar you spend for two weeks. This single habit builds the awareness that makes every other financial skill easier to apply.

How financially literate are Americans in 2025 and 2026?

The data on American financial literacy is sobering. U.S. adults answered only 49% of financial knowledge questions correctly on the 2025 TIAA-GFLEC Personal Finance Index. That score has not moved since 2017. Eight years of financial education campaigns, apps, and resources have produced zero measurable improvement at the national level.

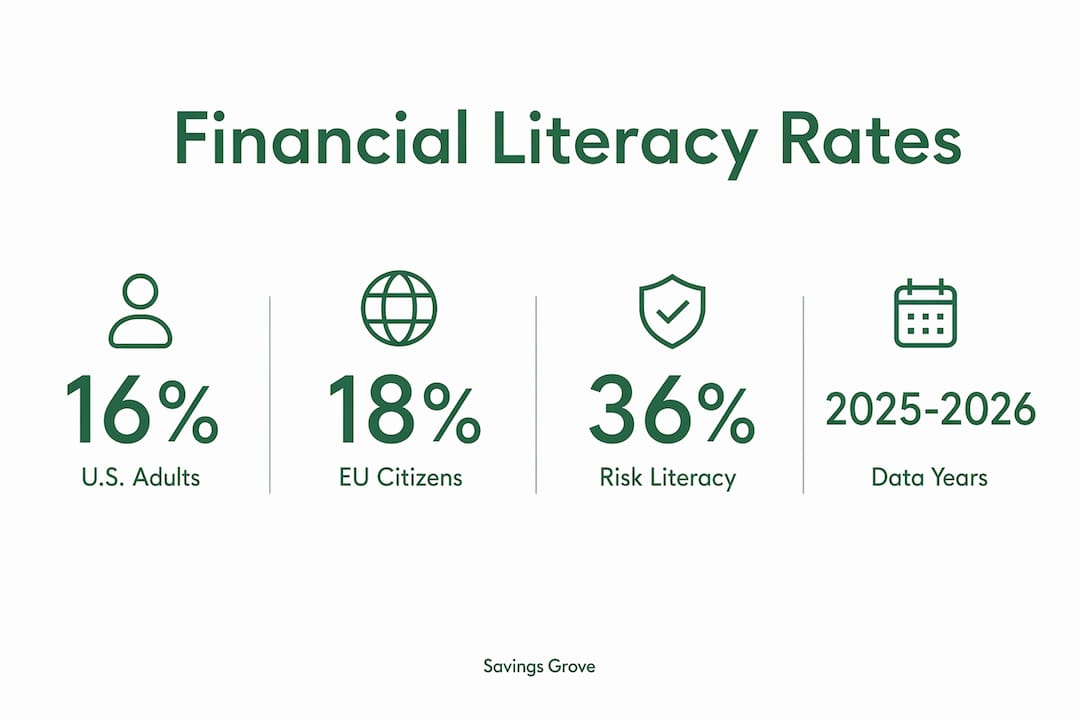

The gaps by demographic group are just as striking. Only 16% of U.S. adults scored high on the index. Women, younger adults, and lower-income households consistently score below average. These are not small differences. They translate directly into worse financial outcomes, including higher debt loads, fewer retirement savings, and greater financial fragility.

Adults with very low financial literacy are 3 times more likely to be financially fragile compared to those with high literacy. Financial fragility means being unable to cover a $2,000 emergency expense within a month.

Risk literacy is declining as a specific concern. Only 36% of adults answered risk-related questions correctly in 2025, down from 39% in 2017. Risk literacy covers understanding insurance, investment volatility, and retirement planning uncertainty. When people misunderstand risk, they make costly mistakes, like underinsuring their home or panic-selling investments during a market dip.

The picture outside the U.S. is not much better. Only 18% of EU citizens have high financial literacy. The Netherlands leads Europe at 28%, but the majority of European adults still score medium or low. Financial literacy is a global challenge, not an American one.

| Population | High financial literacy rate |

|---|---|

| U.S. adults (2025) | 16% |

| EU citizens (average) | 18% |

| Netherlands (EU leader) | 28% |

Why does financial literacy matter for your financial well-being?

Financial literacy directly shapes your financial resilience. Financial literacy underpins financial inclusion and the ability to navigate complex financial products, from credit cards to digital assets. Without it, you are more likely to fall into debt traps, miss out on compound growth, and remain unprepared for emergencies.

The mental cost of low literacy is real and measurable. Low literacy adults spend 10 hours per week worrying about finances. High literacy adults spend about 4 hours. That is 6 extra hours every week consumed by financial stress rather than productive activity. Over a year, that adds up to more than 300 hours lost to worry.

Financial confidence may matter as much as financial knowledge. Combining education with income support produces better financial outcomes than either approach alone.

The benefits of stronger financial literacy include:

- Fewer debt traps: You recognize predatory loan terms before signing.

- Better retirement outcomes: You understand why starting early matters and how to choose appropriate investment accounts.

- Greater resilience: You build emergency savings that absorb financial shocks without derailing your goals.

- Reduced stress: You spend less mental energy on financial uncertainty.

Pro Tip: Financial confidence and financial knowledge reinforce each other. Start with one small win, like paying off a single credit card balance, and let that success build your confidence for the next step.

How to improve your financial literacy skills step by step

Building financial literacy is a process, not a one-time event. The most effective approach starts with the basics and adds complexity over time.

-

Create a written budget. List every source of income and every regular expense. Use a simple spreadsheet or a notebook. Without a structured budget, income increases tend to disappear into higher spending rather than savings or debt repayment. A budget makes that pattern visible and stoppable.

-

Build an emergency fund first. Before investing or aggressively paying down debt, save at least one month of expenses in a separate account. Adults with low financial literacy are 5 times more likely to lack emergency savings. That gap leaves them vulnerable to any unexpected expense.

-

Tackle high-interest debt systematically. List all debts by interest rate. Pay the minimum on everything and direct extra money toward the highest-rate balance first. This method, called the avalanche approach, minimizes total interest paid.

-

Learn one investing concept per month. Compound interest, index funds, and tax-advantaged accounts like 401(k)s and IRAs are the three most impactful concepts for most people. Savings Grove’s guide on money tips for young adults covers these in plain language for readers starting from scratch.

-

Review your financial goals quarterly. Life changes. Income shifts, expenses grow, and priorities evolve. A quarterly review keeps your budget and savings goals aligned with your current reality.

-

Use trusted resources to fill knowledge gaps. Government sites, nonprofit financial counselors, and well-researched personal finance guides give you reliable information. For readers with tighter budgets, Savings Grove’s money tips for low-income Americans addresses practical steps tailored to constrained financial situations.

Pro Tip: Improving financial literacy does not require a finance degree. Reading one credible article per week and applying one idea per month produces real progress over a year.

Building positive financial attitudes matters as much as gaining knowledge. Many people avoid looking at their bank balance because they fear what they will find. That avoidance is itself a financial literacy problem. Developing the habit of regular, calm financial check-ins changes your relationship with money over time. Financial literacy resources focused on financial security practices show that consistent small habits outperform occasional large efforts in building long-term stability.

Key Takeaways

Financial literacy is the combination of knowledge, behavior, and attitudes that determines how well you manage money and make financial decisions over time.

| Point | Details |

|---|---|

| Financial literacy definition | The OECD defines it as knowledge, attitudes, skills, and behaviors working together for sound money decisions. |

| U.S. literacy gap | Only 16% of Americans score high on financial literacy tests, with no improvement since 2017. |

| Low literacy costs | Low-literacy adults spend 10 hours weekly worrying about money and are 3 times more financially fragile. |

| Core skills to build | Budgeting, saving, debt management, and investing form the four pillars of practical financial literacy. |

| Improvement strategy | Start with a written budget, build emergency savings, and add one new financial concept each month. |

Financial literacy is a practice, not a destination

I have spent years reading financial research and talking with people across income levels about money. The single biggest misconception I keep encountering is that financial literacy is something you either have or you don’t. People treat it like a test score. You pass or you fail.

That framing does real damage. It stops people from starting because they feel too far behind. The truth is that financial literacy is a practice, much like physical fitness. You don’t become financially literate by reading one book. You become financially literate by making slightly better decisions this month than you made last month, and then repeating that for years.

The research on stagnant U.S. literacy scores tells me that information alone is not the problem. Most people know they should save more. The gap is in behavior and attitude, not knowledge. That means the most useful thing you can do is not find a better article. It is to take one concrete step today and build from there.

I have also seen how quickly financial literacy compounds. Someone who learns to budget in their 20s does not just save money. They build the habit of tracking, reviewing, and adjusting. That habit pays dividends in every financial decision they make for the rest of their life. The earlier you start, the more that compounding works in your favor. But starting at 40 or 50 still beats not starting at all.

— Mika L.

Savings Grove can help you build financial skills

Managing money gets easier when you have clear, practical guidance in one place. Savings Grove brings together guides on budgeting, saving, debt management, and investing, all written in plain language and updated regularly with current research.

Whether you are just starting to build a budget or looking to close specific knowledge gaps, Savings Grove covers the full range of personal finance skills. The site’s financial diet plan guide walks you through a structured approach to improving your money habits step by step. For readers who want to understand why saving feels so hard, the guide on reasons you struggle to save identifies the real barriers and offers direct solutions. Visit Savings Grove to find the resource that fits where you are right now.

FAQ

What is the financial literacy definition used by experts?

The OECD defines financial literacy as the combination of knowledge, attitudes, skills, and behaviors that enables individuals to make sound financial decisions. It measures literacy across three dimensions: financial knowledge, financial behavior, and financial attitudes.

Why is financial literacy important for everyday Americans?

Low financial literacy is directly linked to financial fragility, lack of emergency savings, and higher levels of financial stress. Adults with very low literacy are 3 times more likely to be financially fragile than those with high literacy.

What does financial literacy include in practice?

Financial literacy covers four main areas: budgeting, saving, debt management, and investing. It also includes understanding risk, reading financial products accurately, and developing positive money habits over time.

How can I improve my financial literacy quickly?

Start by creating a written budget and tracking every expense for two weeks. Then build one month of emergency savings before moving on to debt repayment and investing. Adding one new financial concept per month produces steady, measurable progress.

How financially literate are Americans compared to other countries?

Only 16% of U.S. adults score high on financial literacy assessments, matching the EU average of 18%. The Netherlands leads Europe at 28%. No country has achieved widespread high financial literacy at the population level.