The envelope budgeting method is a cash-allocation system where you divide your income into labeled envelopes for each spending category and stop spending once an envelope is empty. This hard cap is the system’s defining rule. No borrowing from next month, no credit card top-ups. Households that switch from credit card overspending to physical cash envelopes reduce variable spending by 15–20% within three months. That result comes directly from the method’s core mechanic: spending feels real when you hand over physical cash, and that feeling changes behavior. Savings Grove covers this method in depth because it works across income levels, requires no financial background, and costs nothing to start.

What is the envelope budgeting method and how does it work?

The envelope budgeting method, also widely called the cash envelope system, is a zero-friction budgeting framework built on one rule: when the cash in a category envelope runs out, spending in that category stops for the month. You do not need a spreadsheet, a finance degree, or a subscription to make it work. The method eliminates the mental burden of wondering whether a purchase is affordable. If the envelope has cash, you can buy it. If it does not, you wait.

The system targets variable expenses, the categories where overspending is most common. Groceries, dining out, gas, clothing, and entertainment are the usual candidates. Fixed bills like rent, utilities, and loan payments stay on autopay through your bank account. The envelope method does not try to manage those. It focuses its discipline exactly where discipline is hardest.

The psychological benefit is not a side effect. Making spending tangible through physical cash creates cognitive friction that slows impulsive purchases. Handing over a $20 bill registers differently in your brain than tapping a card. That friction is the feature, not a flaw.

How to set up and use envelope budgeting step by step

Setting up the system takes one afternoon. Follow these steps in order and you will have a working budget before the week ends.

-

List your variable spending categories. Experts recommend 3–8 categories for beginners. Common ones include groceries, gas, dining out, entertainment, clothing, and personal care. Do not create a category for every minor expense. Start focused.

-

Review 2–3 months of bank statements. Pull your actual spending history, not what you wish you spent. Calculate a monthly average for each category. This number becomes your envelope amount. Guessing leads to aspirational budgets that collapse within two weeks.

-

Label your envelopes. Write the category name and the monthly dollar amount on each envelope. If you get paid biweekly, split the monthly amount in half and fund each envelope on payday.

-

Fill each envelope with cash. Withdraw the total amount from your bank account on payday. Distribute the cash into each labeled envelope. This physical act of sorting money is where the system starts working on your behavior.

-

Spend only from the correct envelope. Groceries come from the grocery envelope. Gas comes from the gas envelope. No cross-category borrowing unless you make a deliberate, planned transfer and reduce the donor envelope accordingly.

-

Handle leftover cash with intention. At month’s end, leftover cash should go toward a specific goal. Experts recommend directing it toward an emergency fund or debt payoff rather than rolling it into next month’s spending.

-

Review and adjust monthly. Consistent shortfalls in a category are not failure. They are data. Monthly review and reallocation keep the system accurate and sustainable over time.

Pro Tip: Write a running balance on the outside of each envelope every time you spend. Seeing “$47 left, 12 days to go” changes how you make purchase decisions far more than any app notification.

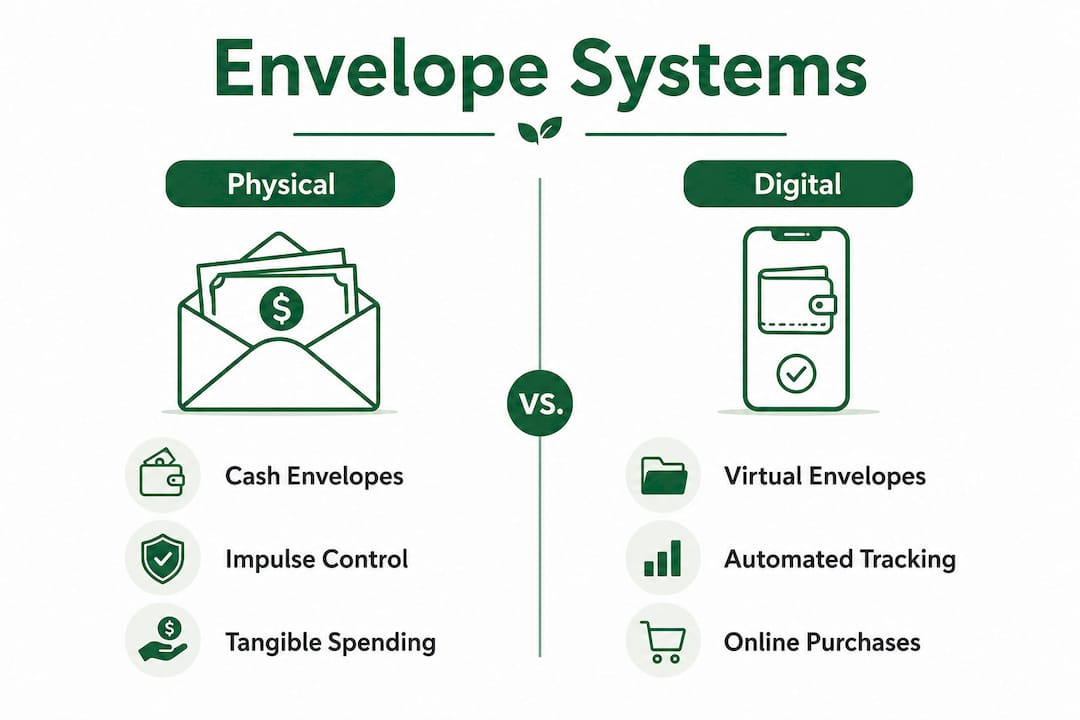

Physical, digital, or hybrid: which envelope system fits you?

The envelope budget system overview looks different depending on how you handle money day to day. Each format has real advantages and real limitations.

Physical cash envelopes

Physical envelopes are the original format and still the most effective for people who overspend on impulse. Handing over cash creates a spending pause that cards and phones do not. The limitations are real: you cannot use cash for online purchases, you risk losing the money, and carrying multiple envelopes is inconvenient.

Best for: People with a history of credit card overspending, beginners who need strong behavioral reinforcement, and anyone who shops primarily in person.

Digital envelope apps

Digital envelope systems create virtual envelopes with hard spending caps. They log transactions automatically, work for online purchases, and eliminate the risk of losing cash. The tradeoff is that digital spending still feels abstract. Tapping a phone to pay does not trigger the same friction as handing over bills.

Best for: People who rarely use cash, frequent online shoppers, and anyone who wants automated transaction tracking.

Hybrid systems

Experienced users keep physical envelopes for their two or three highest-risk overspending categories, such as dining out and clothing, and use digital tools for everything else. This approach captures the behavioral benefit of cash where it matters most while keeping convenience for lower-risk categories.

Best for: Anyone who has tried one format and found it unsustainable, or anyone managing both in-person and online spending regularly.

| Format | Best strength | Main limitation |

|---|---|---|

| Physical cash | Strongest spending friction | No online use, theft risk |

| Digital app | Convenience, auto-tracking | Less behavioral impact |

| Hybrid | Balances discipline and ease | Requires managing two systems |

Savings Grove’s guide to free budgeting apps covers the top digital tools that support virtual envelope categories if you want to explore that route.

Common challenges and how to handle them

Most people who abandon envelope budgeting do so in the first 60 days. The reasons are predictable, and so are the fixes.

-

Aspirational budgeting. Setting a grocery budget of $300 when you actually spend $500 is not discipline. It is a setup for failure. Base every envelope amount on your real past spending, then reduce it gradually over several months if you want to cut back.

-

Running out of money mid-month. This happens. The rule is no borrowing from other envelopes without a deliberate decision. If you transfer $20 from dining to groceries, write it down, reduce the dining envelope visibly, and plan to compensate next month. Untracked transfers destroy the system.

-

Too many categories. Starting with 10 envelopes creates administrative fatigue fast. Begin with 3–5 categories that represent your biggest spending risks. Add categories only after the system feels natural.

-

Forgetting to track. Maintaining a running balance on each envelope, whether written on the outside or logged in an app, shifts spending from passive to active. You make better decisions when you can see exactly what remains.

Pro Tip: If you find yourself raiding envelopes regularly, that category is underfunded, not a personal failure. Adjust the amount and move forward. The system is designed to be flexible.

Adjusting envelope amounts monthly is not a sign the system is broken. It is the system working correctly. Consistent shortfalls mean the allocation was wrong, not that you are.

How envelope budgeting fits with zero-based budgeting

Zero-based budgeting is a framework where every dollar of income gets assigned a specific job, so income minus all assigned expenses equals zero. No dollar sits unallocated. The envelope method is the execution layer that makes zero-based budgeting work in practice for variable spending.

Envelope budgeting applies a hard cap per category, which is exactly what zero-based budgeting needs to prevent overspending after the plan is set. Together, the two approaches create a complete system: zero-based budgeting decides where every dollar goes, and envelopes enforce those decisions in real time.

The practical split looks like this:

| Budget type | What it handles | How it works |

|---|---|---|

| Zero-based budgeting | Full income allocation | Every dollar assigned before the month starts |

| Envelope method | Variable spending categories | Hard cash cap per category, spending stops when empty |

| Automation | Fixed bills and savings | Rent, utilities, and transfers run on autopay |

This combination works especially well for people managing debt repayment alongside daily expenses. Fixed debt payments run on autopay, savings transfers happen automatically, and envelopes control the variable spending that most often derails debt payoff plans. Savings Grove’s weekly paycheck budgeting guide explains how to time these allocations around your pay schedule.

Key Takeaways

The envelope budgeting method works because it turns abstract spending limits into physical, visible boundaries that stop overspending before it starts.

| Point | Details |

|---|---|

| Hard spending cap | Spending stops when an envelope is empty, with no borrowing from other categories. |

| Start with 3–5 categories | Beginning with fewer envelopes reduces burnout and builds lasting habits. |

| Base amounts on real data | Review 2–3 months of bank statements to set realistic, sustainable envelope amounts. |

| Hybrid systems work best long-term | Use physical cash for high-risk categories and digital tools for everything else. |

| Monthly review is required | Consistent shortfalls signal a need to adjust allocations, not a reason to quit. |

Why empty envelopes are the best feedback you can get

I have watched people treat an empty envelope like a personal failure. It is the opposite. An empty envelope at day 22 of the month tells you something specific: either the allocation was too low, or spending in that category was higher than you realized. Both are useful. Neither is shameful.

The part most articles skip is how quickly the behavioral shift happens. Within the first two weeks of using physical cash, most people start making different decisions at the point of purchase. Not because they are more disciplined, but because the money is visibly finite. That visibility does the work.

The hybrid approach is where I see people stick with the system longest. Pure cash is powerful but inconvenient for modern life. Pure digital loses the friction that makes the method effective. Using physical envelopes for the two or three categories where you historically overspend, and digital tracking for the rest, gives you the best of both without the friction of managing everything in cash.

The biggest misconception about envelope budgeting is that it is rigid. The system is actually designed to flex. You can transfer between envelopes deliberately, adjust amounts monthly, and add or remove categories as your life changes. The only thing that does not flex is the core rule: you spend what is in the envelope, and when it is gone, you stop. That boundary is the entire point.

— Mika L.

Savings Grove resources to support your budgeting plan

Envelope budgeting gives you a clear system. Savings Grove gives you the tools and guidance to make it last.

Savings Grove publishes monthly updates on budgeting strategies, financial products, and money-saving resources, all fact-checked and written for real people managing real budgets. Whether you are just starting with envelope budgeting or looking to pair it with the right digital tools, Savings Grove has practical guidance ready. Explore budgeting tips and tools from people who have used these methods to save thousands, or visit Savings Grove to browse the full library of free personal finance resources built for every income level.

FAQ

What is envelope budgeting in simple terms?

Envelope budgeting is a cash-allocation system where you divide your income into labeled envelopes for each spending category and stop spending in that category once the envelope is empty. It works by making spending limits physical and visible.

How many envelopes should a beginner start with?

Beginners should start with 3–5 envelopes covering their highest-risk variable spending categories, such as groceries, gas, and dining out. Starting with too many categories leads to burnout.

Can you use envelope budgeting without cash?

Yes. Digital envelope apps create virtual spending caps that work the same way as physical envelopes, including for online purchases. The tradeoff is that digital spending creates less behavioral friction than handling physical cash.

What happens if you run out of money in an envelope?

Spending in that category stops for the month. If you must transfer funds from another envelope, record the transfer, reduce that envelope’s balance visibly, and plan to compensate in next month’s allocation.

How does envelope budgeting relate to zero-based budgeting?

Zero-based budgeting assigns every dollar of income a specific job before the month starts. Envelope budgeting is the execution layer that enforces those assignments for variable spending categories through hard cash caps.