Credit card tiers are a formal segmentation system that groups cards by benefit levels, fee structures, and rewards potential. The role of credit card tiers is to match cardholders with perks that fit their spending habits and credit profile, while funding those perks through a layered fee structure paid largely by merchants. Understanding how this system works gives you a real edge when choosing a card. Savings Grove tracks monthly updates on credit card products so you can make decisions based on facts, not marketing labels.

How the role of credit card tiers shapes fees and rewards

Credit card tiers function as a cost-transfer mechanism between merchants and cardholders. When you use a premium card, the merchant pays a higher interchange fee to the card network. That fee funds the rewards, travel credits, and insurance protections you receive as a cardholder.

The financial gap between tiers is real and measurable. Stepping up from mid-tier to premium typically raises interchange rates by 0.30% to 0.70%. That increase may seem small, but across millions of transactions it generates enough revenue to cover airport lounge access, concierge services, and cash back programs.

Premium cards represent 20–30% of total cards in circulation but account for 30–45% of total consumer spending. That spending concentration is exactly why networks can afford to offer premium cardholders outsized perks. Merchants absorb the cost, and cardholders capture the value.

The three most common credit card classifications are Standard, Rewards, and Premium. Each tier builds on the previous one in terms of both fees and benefits.

| Tier | Typical Interchange Rate | Key Benefits |

|---|---|---|

| Standard | Lowest | Basic fraud protection, no annual fee |

| Rewards | Moderate | Cash back, points, travel miles |

| Premium | Highest | Lounge access, travel credits, concierge |

Pro Tip: Knowing which tier your card falls into tells you exactly how much value you should expect to extract. If you hold a premium card but never use its travel perks, you are effectively subsidizing other cardholders.

What benefits and rewards actually differ across credit card levels

The benefits gap between tiers is wider than most cardholders realize. Standard cards cover the basics: fraud protection and a credit line. Rewards cards add cash back or points on everyday categories like groceries and gas. Premium cards layer on travel insurance, purchase protection, airport lounge access, and statement credits that can offset annual fees.

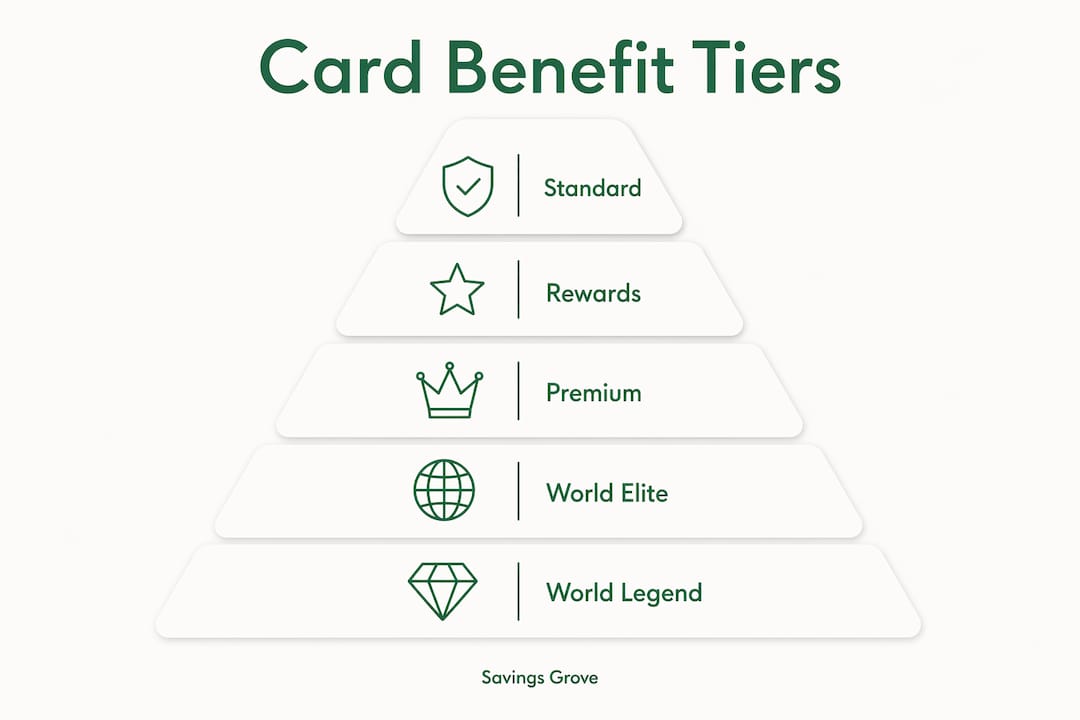

Mastercard structures its tiers as Standard, World, World Elite, and World Legend. Each level includes all benefits from the tier below, then adds incremental perks like travel services and higher statement credits. This stacking model makes it easy to see exactly what you gain by moving up.

American Express takes a different approach. Its card levels reflect spending categories and lifestyle segments rather than a strict hierarchy. A card labeled “Gold” may outperform a card labeled “Platinum” for a specific spender, depending on where they shop and travel.

Common tier-specific benefits include:

- Standard tier: Zero liability fraud protection, basic purchase protection

- Rewards tier: 1%–5% cash back, airline miles, hotel points, sign-up bonuses

- Premium tier: Airport lounge access, trip cancellation insurance, concierge service, annual travel credits, cell phone protection

One critical nuance: marketing labels do not always reflect true tier status. A Visa Platinum card in the U.S. is often an entry-level product with limited benefits, despite the aspirational name. The word “Platinum” signals prestige in marketing, not necessarily in perks.

Pro Tip: Always check the actual benefits guide for any card you consider, not just the name on the front. Two cards with identical tier names from different issuers can have completely different benefit packages.

How to use credit card progression to build credit and unlock better rewards

Credit card progression is the practice of moving from entry-level cards toward premium products over time as your credit score and income grow. It is one of the most practical personal finance strategies available to everyday consumers. Each step up the ladder brings better rewards, higher limits, and stronger protections.

The progression typically follows these stages:

- Start with a secured or student card. These entry-level products report to credit bureaus and build your credit history with minimal risk.

- Graduate to an unsecured rewards card. Once your credit score improves, you qualify for cards that earn cash back or points on everyday purchases.

- Apply for a mid-tier travel or cash back card. These cards offer sign-up bonuses and category multipliers that meaningfully increase your rewards rate.

- Move to a premium card when the math works. Premium cards carry annual fees of $95 to $695 or more. You need to use enough benefits to offset that cost.

- Maintain all cards responsibly. Keeping older accounts open preserves your credit history length, which supports your score over time.

Building a strong credit history unlocks protections that entry-level cards simply do not offer, including trip cancellation insurance, rental car coverage, and concierge services. These protections have real dollar value that compounds over years of use.

Pro Tip: Never apply for a premium card just because you can qualify. Run the numbers first. Add up every benefit you will realistically use, then compare that total to the annual fee.

Common misconceptions about credit card tiers and how to choose the right card

The biggest myth about credit card tiers is that a higher tier always means a better card. Card tiers are specialized product categories, not a simple ranking from worse to better. A premium travel card is the wrong choice for someone who never flies. A flat-rate cash back card at the rewards tier may deliver more value than a premium card loaded with perks you will never activate.

Another common pitfall is ignoring enrollment requirements. Some premium card perks require manual activation to receive benefits like monthly dining credits or streaming service reimbursements. Cardholders who skip this step pay the annual fee without capturing the full value of the card.

Use these criteria when evaluating any card beyond its tier label:

- Match benefits to your actual spending. A card with 4x points on dining is worthless if you cook at home every night.

- Calculate the net annual fee. Subtract the dollar value of benefits you will use from the stated annual fee. A $550 card with $600 in usable credits costs you nothing.

- Check enrollment requirements. Confirm which perks activate automatically and which require you to opt in each month or year.

- Ignore the tier name. Focus on the specific benefits listed in the card’s guide, not the marketing label on the card.

- Review the rewards redemption rules. Points that expire or require a minimum balance before redemption reduce the real value of any card.

The right card is the one that fits your life, not the one with the most impressive name. Aligning your card choice with your actual spending patterns consistently outperforms chasing tier status.

Key takeaways

Credit card tiers work best when you match the card’s benefit structure to your real spending habits, not to a tier label or marketing name.

| Point | Details |

|---|---|

| Tiers fund rewards through merchant fees | Higher interchange rates on premium cards pay for cardholder perks like lounge access and travel credits. |

| Premium cards dominate spending volume | Cards in the top tier represent 30–45% of total spend despite being a minority of cards in circulation. |

| Tier labels can mislead | A “Platinum” label does not guarantee premium benefits; always read the actual benefits guide. |

| Progression builds credit and rewards | Moving from secured to premium cards over time improves your credit score and unlocks stronger protections. |

| Manual enrollment matters | Some premium perks require opt-in activation; missing this step means paying fees without full value. |

My honest read on credit card tiers after years of tracking them

The credit card industry is genuinely good at making complexity feel like prestige. I have watched people carry $695-per-year cards and use exactly one benefit: the airport lounge, twice a year. That is not a premium card strategy. That is an expensive habit dressed up in metal.

What I find most useful about understanding credit card tiers is the clarity it brings to fee math. Once you know that merchant fees fund your rewards, the whole system makes sense. You are not getting something for free. You are capturing a share of a cost that merchants already price into their goods.

The progression strategy is where I think most people leave real money on the table. Starting with a secured card feels unglamorous, but it is the fastest path to qualifying for cards with genuine value. Skipping steps to grab a premium card before your credit is ready usually means higher interest rates and lower approval odds.

My advice: treat your card portfolio like a tool kit. Each card should serve a specific purpose. One card for groceries, one for travel, one for everything else. That approach beats holding one “premium” card that does a mediocre job across all categories.

— Mika L.

Find the right card tier with Savings Grove

Choosing the right card tier gets easier when you have reliable, up-to-date information in one place.

Savings Grove publishes monthly research on credit card rewards and personal finance strategies, so you always know which cards deliver real value at each tier. Whether you are building credit from scratch or ready to move into a premium card, Savings Grove gives you the facts you need to make a confident decision. No guesswork, no outdated comparisons. Just clear, practical guidance updated regularly to reflect the current market.

FAQ

What is the role of credit card tiers?

Credit card tiers segment cards by benefit levels and fee structures, with higher tiers offering more perks funded by higher merchant interchange fees. The system matches cardholders to rewards that fit their spending profile and credit history.

Do higher credit card tiers always offer better value?

No. Card tiers are product categories, not a simple hierarchy from worse to better. The best card depends on your spending habits and which benefits you will actually use.

Why do premium cards cost merchants more?

Premium cards carry higher interchange rates, typically 0.30%–0.70% above mid-tier cards. Merchants pay these fees on every transaction, and that revenue funds the rewards and perks cardholders receive.

What does credit card progression mean?

Credit card progression is the practice of starting with entry-level cards and moving toward premium products as your credit score improves. Each step unlocks better rewards, higher credit limits, and stronger consumer protections.

Why do some premium card benefits require enrollment?

Card issuers require manual activation for certain perks like monthly dining credits or streaming reimbursements. Cardholders who do not enroll miss out on benefits they are already paying for through the annual fee.