Asset allocation is the deliberate distribution of retirement savings across stocks, bonds, and cash to balance growth, income, and risk. For seniors, getting this balance right is not optional. Asset allocation explains up to 94% of portfolio return variability, making it the single most powerful decision you control in retirement. The difference between a portfolio that lasts 30 years and one that runs dry in 15 often comes down to how assets are divided, not which individual stocks you picked.

Why asset allocation matters for seniors more than any other age group

Retirement changes the rules of investing. During your working years, a market drop is an inconvenience. In retirement, it can force you to sell assets at a loss just to cover living expenses. That is why the importance of asset allocation grows sharply once you stop receiving a paycheck.

Historically, US stocks returned an average of 11.5% annually from 1928 to 2026, compared to 4.87% for bonds. That gap matters because inflation erodes purchasing power every year. A portfolio too heavy in bonds may feel safe but quietly loses ground to rising costs over a 20 or 30-year retirement.

Seniors also face a specific threat called sequence-of-returns risk. This is the danger that a major market drop in the first few years of retirement can permanently damage your portfolio, even if markets recover later. Selling equities during early downturns locks in losses and removes shares that would have recovered, shrinking the base that generates future income. A well-structured allocation protects against this by keeping enough cash and bonds on hand so you never have to sell stocks at the worst time.

- Stocks provide long-term growth and inflation protection

- Bonds generate income and reduce short-term volatility

- Cash covers near-term expenses without forcing asset sales

Pro Tip: Calculate how much of your essential monthly spending is covered by guaranteed income like Social Security or a pension before setting your stock-to-bond ratio. That number drives your allocation more than your age does.

How to allocate assets for retirement based on your income floor

The old “age in bonds” rule, which said to hold a percentage of bonds equal to your age, is outdated. Modern frameworks emphasize income floor and spending flexibility over simple age metrics. Holding 70% bonds at age 70 may feel conservative, but it exposes you to inflation risk over a long retirement.

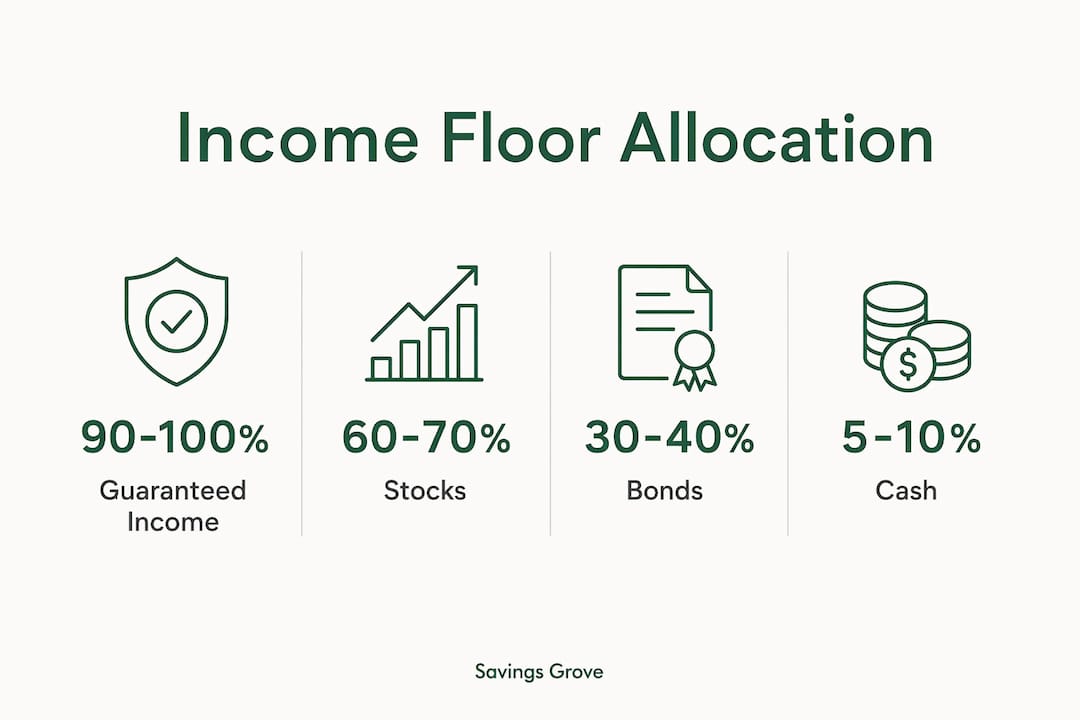

The better starting point is your guaranteed income floor. This is the portion of your essential expenses covered by Social Security, pensions, or annuities. The higher that coverage, the more equity exposure you can safely carry.

| Guaranteed income coverage | Suggested equity allocation | Bond and cash allocation |

|---|---|---|

| 90–100% of essentials | 60–70% stocks | 30–40% bonds and cash |

| 70–89% of essentials | 50–60% stocks | 40–50% bonds and cash |

| 50–69% of essentials | 40–50% stocks | 50–60% bonds and cash |

| Below 50% of essentials | 30–40% stocks | 60–70% bonds and cash |

Retirees with guaranteed income covering 90–100% of essentials can hold 60–70% in stocks without taking on excessive risk. That higher equity share supports growth and helps the portfolio keep pace with inflation over decades.

A typical balanced starting point for a 65-year-old is 50–60% equities, 30–40% bonds, and 5–10% cash. Adjust from there based on your income coverage, health, and spending plans. Portfolios that primarily fund discretionary spending, like travel or hobbies, benefit from higher equity exposure. Portfolios funding essential survival costs lean more conservative.

Pro Tip: Bonds today offer less income than in previous decades. Consider diversifying your bond holdings by duration and credit quality rather than concentrating in one type of fixed income.

Managing market volatility without wrecking your retirement plan

Market downturns are inevitable. The question is whether your portfolio is structured to survive them without forcing bad decisions. If your portfolio drops 10–15%, the recommended response is to pause inflation raises on your withdrawals or trim discretionary spending, not to sell equities.

The bucket strategy is one of the most practical tools for managing volatility. It divides your portfolio into three segments:

- Short-term bucket: 6–12 months of living expenses in cash or money market accounts

- Mid-term bucket: 2–7 years of needs in bonds or stable income assets

- Long-term bucket: Remaining assets in stocks for growth over 7+ years

The bucket approach preserves short-term funds and reduces the pressure to sell stocks during downturns. When markets fall, you draw from cash first and let equities recover.

Rebalancing keeps your allocation on track. Rebalance annually or when allocation drifts by about 5 percentage points from your target. Frequent emotional rebalancing based on market news destroys returns. Pre-set thresholds remove emotion from the process.

Reviews should focus on goals, cash flow, and evolving personal circumstances, not on short-term headlines. A quarterly check-in to confirm your buckets are funded is enough for most retirees.

Pro Tip: Write down your target allocation and your rebalancing rules before the next market drop. Having a written plan makes it far easier to stay disciplined when prices fall.

Practical steps to personalize and maintain your allocation

Building a retirement allocation that works for you starts with knowing your numbers. Follow these steps to get your portfolio aligned with your actual income and spending needs.

- Calculate your income floor. Add up all guaranteed monthly income: Social Security, pensions, and annuities. Compare that total to your essential monthly expenses.

- Set your equity target. Use the income floor table above to determine a starting stock percentage. Adjust based on your comfort with short-term losses and your health outlook.

- Build your cash reserve. Hold 6–12 months of living expenses in cash or a money market account. This is your buffer against forced selling.

- Define your spending buckets. Separate essential spending from discretionary spending. Essential costs need more conservative funding. Discretionary costs can tolerate more volatility.

- Schedule annual reviews. Review your allocation every year and after major life changes like a health event, a spouse’s death, or a significant market move.

- Coordinate with your tax strategy. Place tax-inefficient assets like bonds in tax-deferred accounts and growth assets in taxable or Roth accounts where possible. Time Social Security to reduce the tax burden on withdrawals.

- Avoid over-conservatism. Too much cash feels safe but loses value to inflation. Holding more than 15–20% in cash long-term is a common mistake among seniors that quietly erodes purchasing power.

The most common error in financial planning for older adults is treating the portfolio as a static object. Your allocation should shift gradually as your age, health, and income sources change. Small, planned adjustments beat reactive overhauls every time.

Pro Tip: Keep a one-page record of your current allocation, your target allocation, and the date of your last review. This simple document prevents drift and keeps you accountable.

Key Takeaways

Asset allocation is the primary driver of retirement portfolio outcomes, and seniors who align their allocation with their guaranteed income floor protect both their income and their long-term purchasing power.

| Point | Details |

|---|---|

| Allocation drives returns | Asset allocation explains up to 94% of portfolio return variability. |

| Income floor sets equity level | Higher guaranteed income coverage allows a higher stock allocation, up to 70%. |

| Sequence risk is the top threat | Selling equities during early downturns permanently damages retirement portfolios. |

| Bucket strategy prevents panic selling | Holding 6–12 months in cash removes the need to liquidate stocks during downturns. |

| Rebalance on rules, not emotions | Rebalance annually or when allocation drifts by 5 percentage points from your target. |

The allocation mistake I see most often

Most of the retirees I talk with focus on picking the right investments. They spend hours researching individual stocks or funds. The allocation itself, meaning how much goes into each category, gets far less attention. That is backwards.

The best allocation is not the one with the highest theoretical return. It is the one you can hold through a 30% market drop without selling. Behavioral tolerance is as important as financial capacity. If your allocation keeps you up at night, you will sell at the worst moment, and that single decision can cost you years of retirement income.

I also see too many seniors treat their portfolio as separate from their income plan. Your dividend income, Social Security timing, and withdrawal strategy all interact with your allocation. A 65% stock allocation looks very different for someone with a pension covering all essentials versus someone relying entirely on portfolio withdrawals.

The seniors who retire most confidently are not the ones with the most money. They are the ones who know exactly what their portfolio is supposed to do, why it is structured the way it is, and what they will do when markets fall. That clarity comes from a written, rule-based allocation plan reviewed at least once a year.

— Mika L.

Savings Grove resources for smarter retirement investing

Choosing the right allocation is a starting point, not a one-time decision. As your income needs, health, and market conditions change, your portfolio needs to keep pace.

Savings Grove publishes regularly updated guides on senior investment risk management and low-risk investment options built specifically for retirees navigating today’s markets. Whether you are building your first retirement allocation or adjusting an existing portfolio, the resources at Savings Grove give you clear, research-backed frameworks to work from. Visit Savings Grove to find guides, tools, and practical strategies matched to your retirement stage.

FAQ

What is asset allocation and why does it matter for seniors?

Asset allocation is the process of dividing investments across stocks, bonds, and cash to balance growth and risk. For seniors, it matters because it explains up to 94% of portfolio return variability and directly affects how long retirement savings last.

How much should a 65-year-old have in stocks?

A typical starting point is 50–60% stocks, 30–40% bonds, and 5–10% cash, adjusted based on how much of your essential expenses are covered by guaranteed income like Social Security or a pension.

What is sequence-of-returns risk?

Sequence-of-returns risk is the danger that a major market drop early in retirement forces you to sell assets at a loss to cover expenses. Selling equities during a downturn locks in losses and permanently reduces the portfolio’s ability to recover.

How often should seniors rebalance their portfolio?

Rebalance once a year or whenever your allocation drifts by about 5 percentage points from your target. Rebalancing more frequently based on market news tends to hurt long-term performance.

What is the bucket strategy for retirement?

The bucket strategy divides your portfolio into short-term cash for immediate needs, mid-term bonds for the next several years, and long-term stocks for growth. It prevents forced equity sales during market downturns by ensuring near-term expenses are always funded.