A home buying savings plan is a structured financial roadmap that targets every dollar you need to close on a house, not just the down payment. Most first-time buyers underestimate their total cash requirement by thousands of dollars, which stalls deals at the closing table. The full picture includes your down payment, closing costs, earnest money, and post-purchase reserves. Savings Grove breaks down each component so you can set a realistic target, pick the right savings tools, and build the credit profile that earns you the best mortgage rate.

What are the full cash requirements for buying a home?

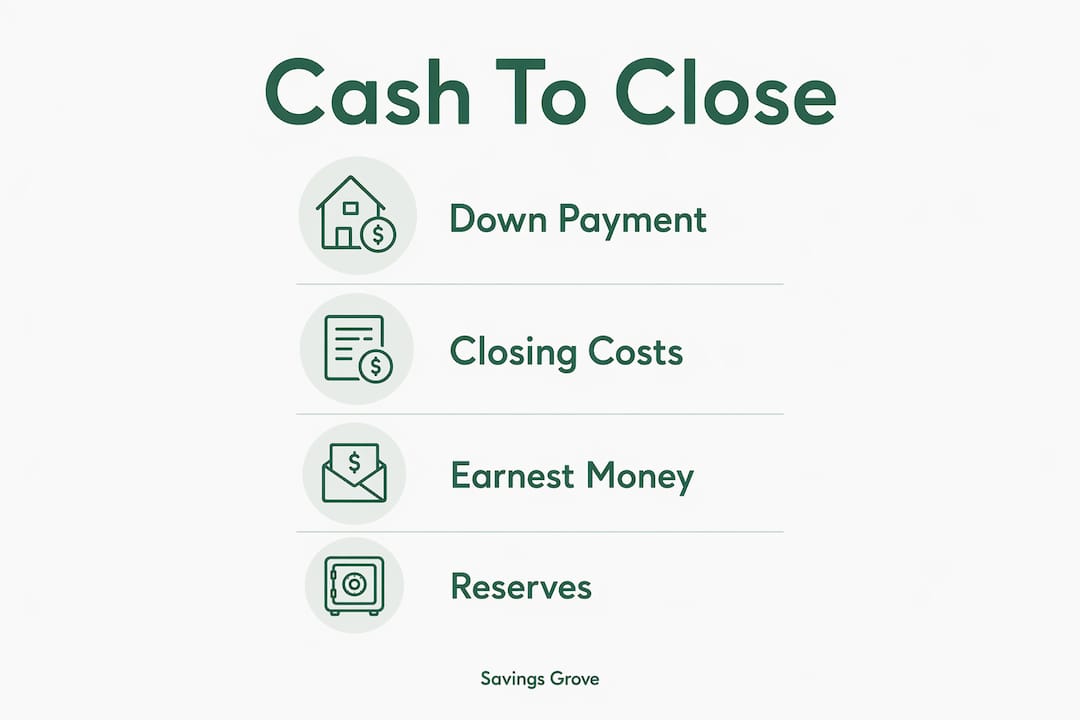

The total cash to close a home purchase covers four distinct buckets: down payment, closing costs, earnest money, and emergency reserves. Treating the down payment as your only target is the most common and costly mistake first-time buyers make.

Down payment

Your down payment percentage depends on the loan type and your goals. Conventional loans allow as little as 3% down, FHA loans require 3.5%, and a 20% down payment eliminates private mortgage insurance. Waiting to reach 20% can price you out of a rising market. A 10% down payment combined with a planned refinance in 5–7 years is often the better path for first-time buyers.

Closing costs

Closing costs add 2–5% of the loan amount on top of your down payment. They cover appraisal fees ($350–$600), home inspections ($350–$1,000+), title insurance, and prepaid escrow accounts for taxes and insurance. For a $350,000 home, closing costs alone can run $7,000–$17,500 depending on your location and lender.

Earnest money and reserves

Earnest money of 1–3% of the purchase price is due when the seller accepts your offer. It counts toward your closing costs, but you need it liquid and ready before closing day arrives. Beyond that, a separate emergency reserve covering 3–6 months of mortgage payments protects you from financial strain caused by immediate repairs or unexpected costs after you move in.

Quick reference: cash requirements at a glance

| Component | Typical amount | When you need it |

|---|---|---|

| Down payment | 3%–20% of purchase price | Closing day |

| Closing costs | 2%–5% of loan amount | Closing day |

| Earnest money | 1%–3% of purchase price | Contract acceptance |

| Emergency reserves | 3–6 months of mortgage payments | Post-closing |

For a $350,000 home, your total liquid cash needed ranges from $35,000 to $50,000 or more. That number clarifies why a down payment savings guide that ignores closing costs leaves you underprepared.

How do you set realistic monthly savings goals?

Setting a monthly savings target starts with one calculation: total cash needed minus current savings equals your savings gap. Divide that gap by the number of months until your target move-in date, and you have your required monthly contribution.

Here is a step-by-step approach to building your timeline:

- Add up your full cash target. Combine your planned down payment, estimated closing costs (use 3% as a conservative midpoint), earnest money, and a 3-month reserve fund.

- Subtract what you already have. Count only liquid savings, not retirement accounts you cannot access penalty-free.

- Divide by your target timeline. If your gap is $30,000 and you want to buy in 30 months, your monthly savings target is $1,000.

- Stress-test the number. If $1,000 per month leaves you unable to cover basic expenses, extend your timeline or adjust your target home price rather than cutting corners on reserves.

- Revisit every quarter. Income changes, windfalls, and expense shifts all affect your pace. A quarterly review keeps your plan current.

Pro Tip: Use a dedicated down payment calculator to model multiple scenarios at once. Changing the home price by $25,000 or the timeline by six months often reveals a much more comfortable monthly target.

Avoid the trap of being overly optimistic about your savings rate. Budget for irregular expenses like car repairs, medical bills, and annual subscriptions before committing to a monthly transfer amount. A plan you can actually sustain beats an aggressive plan you abandon in month three.

What are the best savings vehicles for a home down payment?

Where you keep your savings matters as much as how much you save. The right account depends on your timeline.

For timelines of 0–2 years, capital preservation is the only goal. High-yield savings accounts and money market funds currently offer 4–5% APY, are FDIC insured, and keep your money fully liquid. You can withdraw without penalty the moment you need funds for earnest money or closing costs.

For timelines of 2–5 years, certificates of deposit (CDs) and Treasury bills offer slightly higher yields in exchange for locking your money for a fixed term. A CD ladder, where you stagger maturity dates every 3–6 months, gives you periodic access to funds without sacrificing all of your interest earnings.

For timelines beyond 5 years, a portion of your savings can go into a diversified stock portfolio. Market volatility is manageable over longer periods, and the growth potential outpaces savings account rates. Still, move funds into a high-yield savings account 12–18 months before your target purchase date to protect against a market downturn at the worst possible time.

Pro Tip: Open a savings account with a different bank than your everyday checking account. The small friction of transferring money between banks reduces impulse spending from your house fund.

The single rule that applies to every timeline: never put short-term home savings into individual stocks or cryptocurrency. The risk of capital loss on a 1–2 year horizon is too high to justify any potential upside.

How do disciplined saving habits and credit health lower your mortgage costs?

Automating your savings and managing your credit score work together to reduce the total cost of your mortgage. Neither alone is enough.

Automation removes the decision from your hands. Set up an automatic transfer from your paycheck to your dedicated house fund on payday. Diverting savings before they reach your checking account is the most reliable way to protect your savings discipline. When the money never appears in your spending account, you cannot spend it.

Budgeting identifies the cash you did not know you had. Review three months of bank and credit card statements and categorize every expense. Most households find 10–15% of their spending goes to categories they can reduce without affecting quality of life. Subscriptions, dining out, and impulse purchases are the most common targets. Redirecting even $200 per month adds $2,400 to your house fund annually. For more ways to free up cash, the expense-cutting strategies at Savings Grove give you a practical starting point.

Your credit score directly controls your mortgage interest rate. Keeping credit utilization below 10% and raising your score above 740 qualifies you for the best mortgage rates available. A lower rate reduces your monthly payment and your total interest paid over the life of the loan. That difference can be tens of thousands of dollars.

- Pay every bill on time. Payment history is the largest factor in your credit score.

- Keep credit card balances well below their limits. Aim for under 10% utilization on each card.

- Avoid opening new credit accounts in the 12 months before applying for a mortgage.

- Monitor your credit report for errors. Dispute inaccuracies immediately since they can drag your score down unfairly.

- Check your credit score impact on mortgage affordability before you start the application process.

Pro Tip: Request your free credit reports from AnnualCreditReport.com and review all three bureaus. Errors appear on one bureau but not the others, so checking all three catches every problem.

What financial preparations keep you stable after closing?

Buying the home is the beginning of your financial commitment, not the end. The months immediately after closing carry the highest risk of financial strain.

Your emergency fund must stay completely separate from your down payment savings. Homeownership is liquidity-intensive, and a single unexpected repair can become a financial crisis if you have no cash reserves. Maintain 3–6 months of mortgage payments in a dedicated emergency account before and after you close. The Savings Grove guide on building an emergency fund walks you through the process step by step.

Budget for immediate post-closing costs that most buyers overlook:

- Moving expenses and utility deposits

- Appliance replacements or repairs not covered in the sale

- Landscaping, paint, and cosmetic updates

- New locks, security systems, and basic safety upgrades

Your monthly housing budget must account for more than the mortgage payment. Total monthly housing costs including mortgage, property taxes, homeowner’s insurance, and utilities should not exceed 30% of your gross monthly income. Staying within that threshold keeps homeownership affordable and leaves room for savings and unexpected expenses.

Focus on your personal comfort zone rather than the maximum amount a lender will approve. Lender approval limits reflect what you can technically borrow, not what you can comfortably repay while maintaining your quality of life. Buying below your approval ceiling is one of the most protective financial decisions a first-time buyer can make.

Key Takeaways

A complete home buying savings plan targets down payment, closing costs, earnest money, and emergency reserves together, not the down payment alone.

| Point | Details |

|---|---|

| Know your full cash target | Total cash needed for a $350,000 home ranges from $35,000 to $50,000 or more. |

| Set a monthly savings goal | Divide your savings gap by your timeline in months to find your required monthly contribution. |

| Choose the right savings account | Use high-yield savings accounts or money market funds for timelines under two years. |

| Automate every transfer | Move savings to a separate account on payday before the money reaches your spending account. |

| Protect your credit score | Keep credit utilization below 10% and target a score above 740 for the best mortgage rates. |

What I have learned from watching buyers get blindsided at closing

By Mika L.

The single most damaging belief I see among first-time buyers is that saving for a house means saving for a down payment. That belief has derailed more purchases than bad credit or rising rates combined. Buyers show up at closing with a solid down payment and then discover they are $8,000 short on closing costs and earnest money. The deal falls apart, and months of work disappear.

The fix is simple but requires a mindset shift. Think in terms of cash to close, not down payment. Every savings target you set should reflect the full number, including reserves. When you plan for the complete picture from day one, you avoid the panic that comes from discovering new costs at the worst possible moment.

I also believe most people underestimate how much automation changes their behavior. Moving money to a separate bank account before you see it in your checking account is not a trick. It is the most reliable savings mechanism available to anyone without a financial advisor. The money you never see is the money you never spend.

One more thing: do not sacrifice your emergency fund to accelerate your down payment. A home without cash reserves is a liability, not an asset. Owning a house that one broken furnace or roof leak can destabilize financially is not the goal. Build both funds in parallel, even if it extends your timeline by a few months.

— Mika L.

How Savings Grove supports your path to homeownership

Savings Grove gives you the research-backed tools and practical guides to put your home savings strategy into practice without guesswork.

Whether you are calculating your full cash-to-close target or looking for ways to free up more money each month, Savings Grove has you covered. The site’s proven savings strategies help you build your house fund faster, while the money tips for homeowners section prepares you for the costs that come after closing. Every resource is updated regularly with current rates and real-world examples so your plan stays accurate as the market changes.

FAQ

How much cash do I need to buy a $350,000 home?

Total liquid cash for a $350,000 home typically ranges from $35,000 to $50,000 or more. That figure includes the down payment, closing costs of 2–5%, earnest money of 1–3%, and a post-closing emergency reserve.

What is the fastest way to save for a house?

Automate a fixed transfer to a dedicated savings account on every payday before the money reaches your checking account. Pair that with a monthly budget review to redirect discretionary spending toward your house fund.

Should I invest my down payment savings in stocks?

Only if your home purchase is more than five years away. For timelines under two years, keep savings in FDIC-insured high-yield savings accounts or money market funds to protect against market volatility.

What credit score do I need for the best mortgage rate?

A credit score above 740 qualifies you for the most competitive mortgage rates. Keeping your credit utilization below 10% is one of the fastest ways to push your score into that range.

How much should I keep in an emergency fund after buying a home?

Maintain 3–6 months of mortgage payments in a separate emergency account after closing. This reserve covers unexpected repairs and prevents a single expense from threatening your ability to make mortgage payments.